Articles

See All

A TURNAROUND STORY WITH MOMENTUM AT ITS BACK D-BOX TECHNOLOGIES (DBO – TSX)

![]()

D-Box Technologies has always been a customer experience company with a compelling product. But for years, the experience of owning D-Box stock was been anything but!

This is a stock that I have watched seemingly forever! Until only recently, there was never a reason to act on it.

D-Box was one of those companies where the big turn was on the horizon but it never seemed to materialize.

Yet their product is compelling. When you sit in a D-BOX seat at the movies, the chair moves with the film. It tilts, vibrates, and rumbles in sync with the action on screen. The experience is genuinely different.

Source: D-Box Press Release

QUICK FACTS

Trading Symbols: DBO

Share Price Today: $0.90

Shares Outstanding: 222.7 million

Market Capitalization: $200 million

Cash: $16.2 million

Debt: $0.4 million

Enterprise Value: $185 million

But still… the performance of the stock was just not good. Nevertheless, even I was surprised to learn that, until the recent inflection, which is the reason for this piece, D-Box had 23 years of not being profitable. Yeesh!

The problem was that D-Box kept chasing new verticals — home entertainment, VR, arcade, gaming — pouring their high-margin theatre royalties into failed consumer hardware experiments and bloated overhead

You just kept hoping the company would stop wasting what they had!

Then it happened. D-Box turned the corner in 2024 and it hasn’t looked back since.

Source: Stockcharts.com

Years of…varied…focus…have now narrowed on a single vertical and high margin royalty revenue.

For that turnaround we can thank activist investor Daniel Marks and his fund Stonehouse Capital Management.

Marks got the ball rolling. He began buying D-Box stock in 2021. He really came on the scene a couple of years later when he publicly criticized management and submitted a formal shareholder proposal demanding a special committee of independent directors to review strategic alternatives including a sale of the company.

Marks’s prior activist campaigns at Intrinsyc Technologies, Pacific Safety Products, and MTI Global each ended in a sale at a premium. But after that initial engagement at D-Box, he chose a different path — installing new management and refocusing the business.

Marks had intuited two main points. First, that the diamond in the rough was their royalty business. Second, if D-Box wanted to focus on royalties they needed to focus on theatres.

By the summer of 2024, Marks’s campaign had driven significant board changes. Marks pushed and succeeded in an entire turnover of the management team. By June 2025, there was a new CEO — Naveen Prasad. By August 2025, a new CFO — David Reid.

And a new focus. D-Box is now being run now with royalties front and center, and with a focus on putting their product in theatres.

Of course, as the chart plainly shows, the stock has already had a big move. This was a 20c stock in the summer. It is close to 90c now.

Which means that caution is warranted. But the turnaround appears to be real, and that means this first move up may just be the first movement in a much longer run.

SELLING MOTION

D-BOX makes haptic/motion actuators. What is that English? Seats that move.

D-Box seats can vibrate, rotate, and provide textural feedback in sync with any media source. Think motion seats in movie theatres, or simulation rigs for training.

Their manufacturing facility is in Longueuil Quebec.

D-Box doesn’t manufacture the finished seat product. Their expertise is focused on the technical elements. That starts and ends with the actuators, which use a combination of gears and motors to drive the motion and create the movement of the seat.

Source: D-Box Haptic Actuator and Bridge

The actuator is orchestrated by software, which D-Box also develops. Sounds and action are hand-encoded to link to motion effects. This isn’t something that can be vibe-coded. This is largely “hand-encoded” and has to be customized to the experience, either to a movie or video game or training session, frame-by-frame.

For interactive content (games), D-Box engineers build out a whole library of motion responses tied to in-game telemetry – every motion that you can make has to be choreographed.

The resulting content library is part of their moat. As of January 2025, D-Box estimated that their content catalogue covers over 2,500 films and TV series.

GOING TO THE MOVIES

For years D-Box was pulled in too many directions. They were trying sell their haptic devices into professional simulation, movies, arcade, VR, home entertainment, gaming, racing simulation, commercial racing, heavy equipment, defense, aerospace, and agriculture.

They were spread too thin. And most of these verticals were one-time hardware-only sales.

What Marks recognized is that one of these markets – movies and theatres – gave D-Box the opportunity to drive a recurring revenue stream that would be valued more by investors and let the company build growth over years by structuring the sale with a royalty.

With Marks urging D-Box has made the transition to focus on selling into verticals that will drive more royalties. And that has meant focusing on theatres.

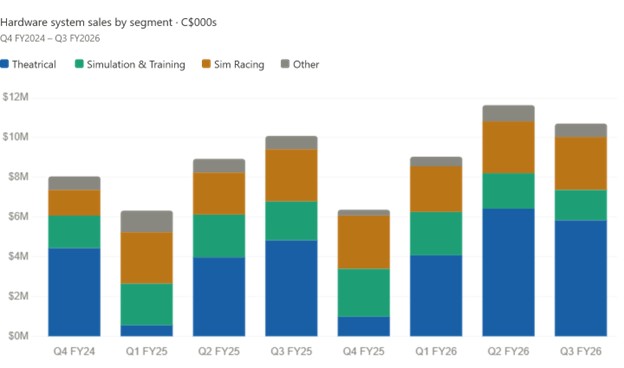

The segment, which D-Box calls their theatrical segment, is already their largest. Hardware sales alone from Theatrical are more than Simulation and Training and Sim Racing combined.

Source: D-Box Financials

The royalty model levers D-Box directly to the demand of the product by theatregoers.

When a patron sits in a D-Box seat, they pay an upcharge over the standard ticket price. This premium is typically $5-8 above a standard ticket. D-Box takes a cut of that upcharge.

Royalty margins are nearly all upside, with over 80% gross margins or higher as utilization goes up. Content costs are already sunk once a film is motion coded so every additional screen goes almost entirely to the bottom-line.

But this is different than a SaaS business. D-Box is only getting paid on usage. If things go badly for the theatre, or if the movies coming out simply aren’t that popular, D-Box takes the hit directly.

Source: D-Box Financials

For the full fiscal year 2025, royalties reached $11 million, accounting for 26% of the company’s revenue mix, on total record revenues of $42.8 million, up 8% year-over-year.

And they may just be getting started. Theatrical is a very big market.

WHO ARE THEIR CUSTOMERS

First, let’s focus on the theatrical customers. D-Box is in 1,047 active screens as of Q1 fiscal 2026. Against the global total that’s roughly 0.5% of all screens worldwide — a tiny fraction.

Even against just North America’s 42,000 screens, D-Box is in perhaps 400-500 screens, which is still only about 1%.

Their most important theatrical customer has been Cinemark. D-Box has installed their haptic technology in more that 325 Cinemark auditoriums globally.

Cineplex is another long-time customer. They have over 3,000 haptic seats in over 100 theatres.

Hoyts is a large movie theatre owner in Argentina, Australia and New Zealand. They have haptic seats installed in at least 32 theatres. In the summer they announced plans to add 539 haptic seats from D-Box across 19 screens.

D-Box has one significant customer in their Sim Racing segment – F1 Arcade.

Sim Racing has gone from niche hobby to commercialized e-sport. It is a B2B business. They aren’t selling the equivalent of gaming consoles to consumers. These are large simulators used at venues.

F1 Arcade is a one-stop shop for food, drinks, and F1 simulator racing, creating unforgettable memories in a casual and inclusive atmosphere — including Race Weekend Watch Parties. D-BOX is the exclusive official supplier of haptic systems to F1 Arcade.

F1 Arcade is expanding aggressively. They have locations in Boston, Washington D.C., Philadelphia, Denver, Las Vegas, Atlanta, the U.K., and Spain. Their growth strategy is pursuing licensing of their compact “F1 Box” format to hotels, casinos, airports, cruise ships, and shopping malls worldwide.

Every new F1 Arcade location is a likely D-BOX hardware sale.

D-Box’s Simulation and Training segment targets the construction, automotive and military industries. They are used by Caterpillar, John Deere, and CM Labs Simulations, and some US military training facilities.

The biggest customer in this space is CM Labs.

CM Labs is a Montreal-based company with over 25 years of experience and more than 1,200 simulator installations across 42 countries, positioning itself as the global leader in heavy equipment simulation training for construction, utilities, and ports markets.

CM Labs is a software simulator design company. They have been integrating D-BOX technology since 2011 to provide the physical feel of operating a crane or excavator.

CM Labs core product is the Intellia Workforce Training System, which combines high-fidelity simulators, curriculum, and training management software.

On the military side, Precision Flight Control is another long-time customer. PFC is a manufacturer of FAA-approved flight training devices covering general, commercial, and military aviation. Their customer base includes NASA, the US Air Force, the US Forest Service, as well as industry primes like Northrop Grumman, Lockheed Martin, and Boeing, and institutions like Embry Riddle University and the US Navy.

Military is a sticky vertical. Aviation and military training carry higher regulatory requirements and longer procurement cycles, which means once D-BOX is embedded in a certified PFC simulator, switching costs are very high.

WHAT’S THE MARKET PRICING THE STOCK AT?

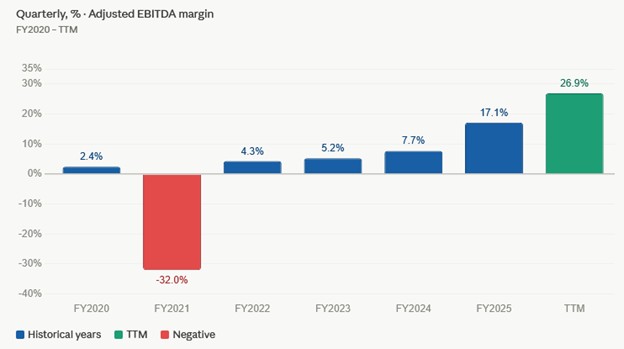

The turnaround in D-Box over the last couple of years has been dramatic. The company went from perennial single digit EBITDA margins to something close to 30%!

Source: D-Box Financials

Of course, over the past 9 months the stock has also quadrupled.

Today, D-Box trades at 13x trailing EV/EBITDA and 13x P/E.

The earnings number is a bit skewed because D-Box hasn’t had to pay taxes and in the last quarter they had a large, deferred tax recovery last quarter.

It may be more accurate to just look at the cash. D-Box generated about $11 million of free cash flow in the last 12 months, an impressive amount. They trade at 18x P/FCF.

This isn’t a bargain valuation, nor should it be. They reflect the success that D-Box is seeing – the turnaround is well in the making. This is no longer a marginally profitable business just barely getting by.

The more interesting question is whether the current valuation prices in the royalty growth ahead. It likely does not. D-Box is well-loved by the online crowd, and they argue that comparable high-margin, recurring revenue businesses trade at 20–30x earnings.

I would agree. D-Box at 13x, with a screen count at 0.5% of global inventory and a new management team actively signing new deals, looks like it could be in the early innings of a multi-year re-rating.

What is going to determine the fate of the stock in the short run is going to be the box office.

Source: D-Box Technologies Investor Presentation

This has a chance to be a year of blockbusters. The first of these, Super Mario Brothers, should begin impacting D-Box results in their 2027 fiscal Q1. At the end of March Super Mario Brother came out. The Mandalorian movie comes out at the end of May, Spiderman in July, and the Avengers in December.

On top of that, there are plenty of other movies coming out of course, these are just the biggest. D-BOX works closely with producers in Hollywood to sync all the epic moments to their haptic seats and designers hand-code every major release.

One big risk is a weak studio slate, or another COVID-style disruption to theatrical attendance, which would hit royalties hard.

On the flip side, a blockbuster movie season in 2026 could be the next catalyst to move the stock. The royalty model is simple and compelling. Sell hardware to get seats into cinemas. Earn a cut of every ticket sold in those seats, forever, at nearly 100% incremental margin. Grow the screen count. Repeat.

With continued earnings growth, it’s easy to see the valuations stretching further as D-Box builds on their success.

Get ready for our next subscriber pick—-SUBSCRIBE HERE