Articles

See All

Growing Revenue and EBITDA…and UnLoved

ZEFIRO METHANE ZEFI-CBOE / ZEFIF-OTC

When one of my top contacts in the industry said I should look at Zefiro Methane last week, I nearly choked.

I helped them get public, I was a seed shareholder–and then I just saw the 1. odd sounding press releases 2. financials show money going out the door 3. management interviews that were vague on details…

But I hadn’t paid attention for a while. In the last year, new CEO Catherine Flax has to a large degree cleaned house after a big public proxy fight with founder Talal Debs, brought in new capital from her network, and allowed operator Luke Plants to show what he can do.

After reading through all the press releases, I realized…

A. the company had stopped most of the financial bleeding,

B. and was not only increasing revenue

C. but actually generating positive EBITDA.

D. Here was a company with a somewhat unique business model–adding carbon credits onto plugging old oil wells–and being successful at it. A differentiator.

E. CEO was clearly very committed after such a public proxy fight, and had got her network to start funding the company.

F. Trading at 1x sales.

G. Everyone I talked to about the company….hated it.

H. Stock chart looking good.

I. Oil Field Services (OFS) stocks have actually done well in the last year (see my PHX Energy!!!). Two years ago when this went public, nobody cared about OFS stocks. Now they’re on the front page. And this company is performing, and it’s under the radar,and in whatever radar it is on, it’s unloved.

PERFECT SET UP.

I still have a lot of questions, and I’m not scheduled to speak with Catherine until next week. Also, the next quarterly is out in the next two weeks, which will cover Jan-Feb-Mar 2026, and the proxy fight was resolved in March, so there is likely to be a lot of important updates on the balance sheet and business updates then.

After my call with her, and the quarterly, I’ll update the report.

Overview

Zefiro Methane Corp. (Cboe Canada: ZEFI | Frankfurt: Y6B | OTCQB: ZEFIF) is a rare hybrid – part oilfield-service operator, part carbon-credit originator. It makes money by plugging and sealing old oil and gas wells, measuring methane leaks, and converting those emissions savings into verified carbon credits.

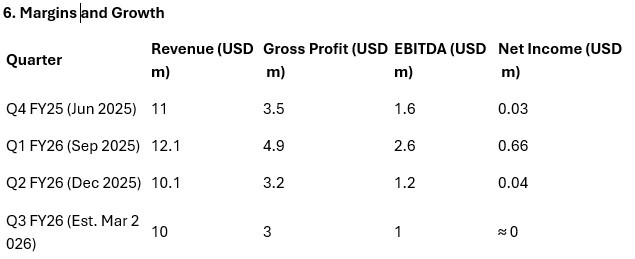

Headline Numbers

• Estimated well-cleanup market: $400-600 billion (U.S. + Canada)

• Revenue run rate (FY 2026): $40 million

• Gross margin: ~36% and rising

• Adjusted EBITDA: $3.8 million first half FY 2026

• Net income: Positive for two straight quarters

1. The Unplugged Well Problem

North America has more than 2.5 million orphaned oil and gas wells – 2.2 million in the U.S. and roughly 130 thousand in Canada. These wells continue to leak methane, which traps ~80× more heat than CO₂ over 20 years.

It costs $100 000-$150 000 per well to close properly, meaning an addressable remediation market north of $400 billion. For decades, very few were fixed because:

• Old operators vanished, leaving no liable owner.

• Regulation was patchy and enforcement weak.

• Plugging gear was costly and slow.

• There wasn’t public money – until 2021’s U.S. Infrastructure Investment and Jobs Act (IIJA) funded $4.7 billion in state grants.

That federal funding is now hitting the ground, giving Zefiro an insured, multi-year pipeline of projects. The firm currently wins about 30-35 % of Phase 1 grant awards in Ohio.

2. Plugging Muscle: Plants & Goodwin (P&G)

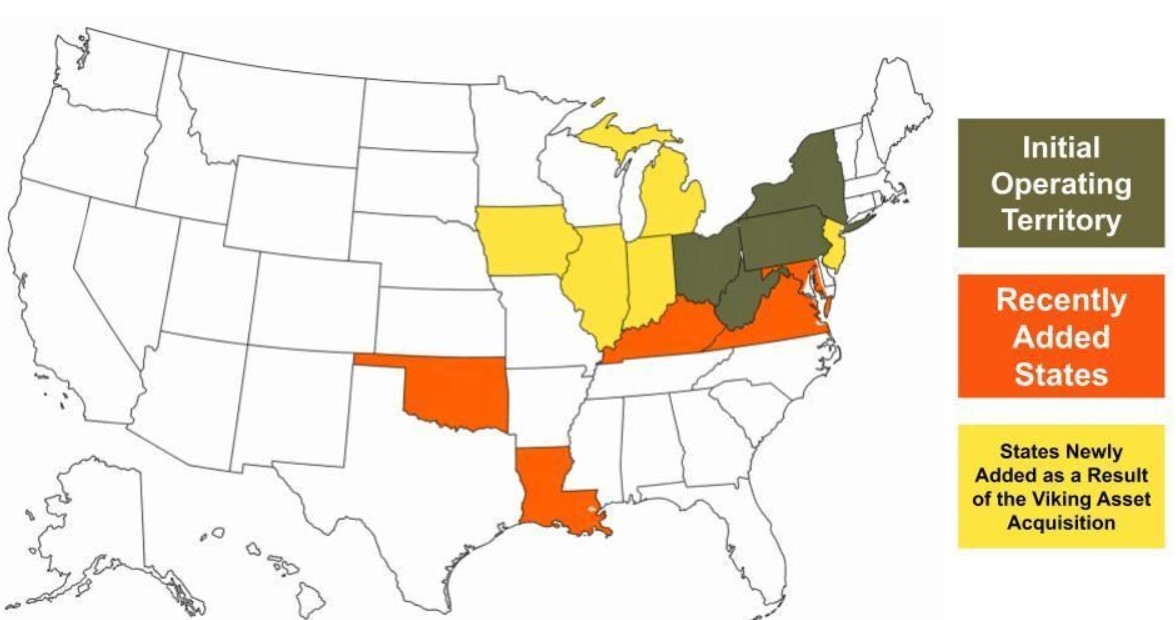

Bought in 2023, Plants & Goodwin (P&G) is a Bradford, Pennsylvania company with five decades of well-plugging experience. Its reputation and permits instantly made Zefiro a top-tier government contractor. Today P&G runs six active rig crews across eight states and is expanding into Louisiana and Oklahoma.

Key projects:

• $19.6 million three-year CMAR contract for Ohio Department of Natural Resources.

• Wood 12F (Ohio) – $4.5 million, 37 wells plugged.

• $5 million private-sector job in Louisiana completed three weeks early.

3. Zefiro’s Technology Edge

Wellhead Containment Tool (WCT) – Patent Pending

Methane measurement at an orphan well is notoriously unreliable. Temperature shifts, wind, and leaky joints cause erratic readings that can invalidate carbon-credit certification. Zefiro’s engineers built a portable composite dome that clamps air-tight over the steel wellhead, isolates a fixed cubic-foot volume of atmosphere, and channels gas into flow sensors.

How it works and why it matters:

• Creates a sealed “micro-lab” at the well mouth; readings stabilize within seconds.

• Compatible with infrared and catalytic sensors; no external power needed.

• Cuts field time per well by ~40 %.

• Enables verifiable methane baselines, a prerequisite for ACR credit approval.

• Reduces crew exposure to raw gas and windborne debris.

Every unit is hand-built from light aluminum and fiberglass; six crews now deploy them daily. In its first full quarter of use, WCT lifted methane-monitoring gross margins from ~25% to ~50%. Zefiro plans to license the tool to other environmental contractors in 2027.

REED Downhole Casing Expansion Tool

Through its exclusive U.S. license with Radial Casing Solutions (RCS), P&G uses the Radial Elastomer Expansion Device (REED) – a patented hydraulic system that expands steel casing from inside the well.

In practice:

1. A hydraulic mandrel pushes an elastomer sleeve outward under high pressure.

2. Steel casing walls stretch a few millimeters to seal microscopic cracks & corroded joints.

3. Methane, brine, and gas vent paths close without re-cementing the entire well.

Average cost per repair: $20 000-$30 000 versus $100 000 for a full re-drill. That difference lets Zefiro bid more aggressively and still earn 20-30% EBITDA margins per contract. REED also forms part of its optional “turn-key P&A package” marketed to private operators.

P&G is the only U.S. holder of the REED patent license. No competitor can use the tool without sub-licence from Zefiro, providing a clear commercial moat.

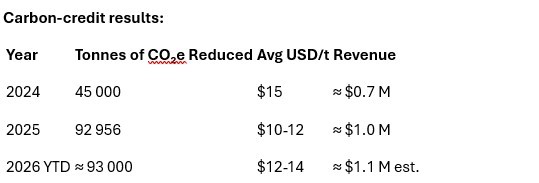

4. The Carbon-Credit Flywheel

Zefiro converts methane-abatement data from those same wells into carbon credits under the American Carbon Registry (ACR). It was the first company to earn credits under ACR’s 2023 “orphan well” method.

Credits have been sold to Mercuria Energy America, EDF Trading, and World Kinect Energy – all blue-chip buyers. Each credit represents one tonne of CO₂ equivalent eliminated, and prices rise with verified quality and U.S. origin.

An updated ACR method due in late 2026 will standardize multi-well projects, which could double Zefiro’s annual credit volume to ≈ 200 000 tonnes.

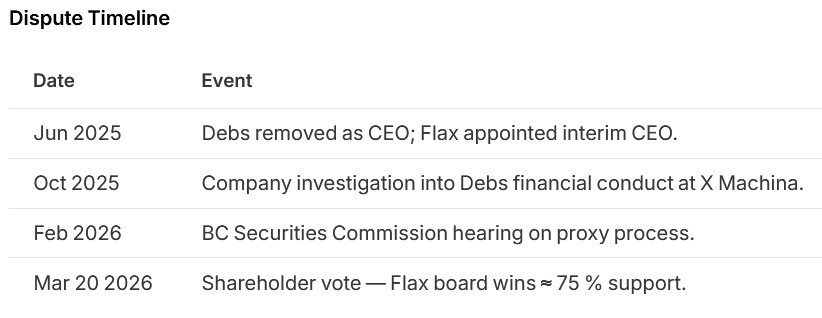

5. The Boardroom Battle and the Turnaround

The Conflict

Founder Dr. Talal A. Debs ran Zefiro until June 2025. He wanted to build a data-science-driven “carbon intelligence platform” around satellite well detection and environmental analytics. Meanwhile revenues flattened and debt mounted.

The board installed Catherine Flax, then a director, as interim CEO and later permanent. She came from J.P. Morgan and BNP Paribas commodities desks with a clean fix-focus: cut overhead, stabilize cash flow, grow verified operations.

Debs responded with a proxy fight backed by X Machina Capital in early 2026. He accused Flax of diluting existing holders and “gutting innovation.” The dispute spilled to the British Columbia Securities Commission, but the March 20, 2026 shareholder vote went overwhelmingly in Flax’s favor. Her team remains secure.

The Fix-It Plan

Flax moved fast once in charge:

1. Cut corporate overhead by nearly 50%. Head-office headcount dropped from 26 to 12; PR and consulting spend was halved.

2. Renegotiated debt. Retired $2.8 million of 12% short-term notes using free cash flow and a lower-rate $300 000 bridge due 2027.

3. Streamlined subsidiary operations. Merged duplicative administration between P&G and the parent. All accounting now consolidated in a single ERP system.

4. Asset discipline. Sold 3 idle rig trailers and spare vehicles for $400,000 cash; entered new rental agreements instead of buying equipment upfront.

5. Stopped non-core R&D. Debs’s satellite mapping projects and AI spending (~$700 000 a year) were closed immediately.

6. Reworked management pay. Shifted half of executive comp into performance shares vesting after three years.

These moves cut quarterly operating expenses to $3.1 million from $4.4 million the year before – saving $1.3 million per quarter and turning cash flow positive within six months. She is clearly willing to make tough decisions quickly and execute.

Catherine Flax: From Wall Street to Well Sites

Flax’s career reads like a checklist for a transition-era CEO.

• J.P. Morgan: Former Global Head of Commodities EMEA & CEO of Commodities in London.

• BNP Paribas: Ran Commodity Derivatives for the Americas.

• Abaxx Technologies: Current Board member; its shares have roughly tripled since 2023 as it builds a digital LNG and carbon futures exchange.

• X Machina Capital: Founding President of Private Markets division before splitting with Debs.

That mix gives her credit in both energy finance and new carbon trafficking – a perfect fit for Zefiro’s hybrid model.

Under her leadership, Zefiro cut operating costs by nearly 50 percent year-over-year, cleared $3 million of short-term debt, and turned two consecutive profitable quarters to close 2025.

Methane monitoring projects deliver roughly 2× the margin of plugging jobs, so as those scale – and carbon credit sales build – Zefiro should see gross margin > 40% and net 10-12% in 2026-27.

Zefiro remains the only public company vertically integrated from plugging through carbon-credit origination in North America.

8. The Investment Case

Catalysts:

• New state contracts in Ohio and Louisiana pipeline.

• Doubling of methane-monitor fleet (12 crews by 2027).

• Upcoming ACR method update boosting credit output.

• Potential licensing of Wellhead tool to peers.

Risks: Carbon offset price volatility; delays in ACR approvals; federal funding cycles.

Base case: FY27 revenue US$60-65 million, EBITDA US$8-10 million. Balance sheet net-debt free within 18 months.

The oil field services sector is still very fragmented, and Flax & Plants have been active on the M&A front, recently buying Viking Well Services who has been active in different states than Zefiro. Mostly in Appalachia (Marcellus formation), Zefiro is now active in Louisiana and some mid-continent states as well.

A wild card would be full Democratic control of both the Senate and the House in this November’s mid-term elections in the US. I have to believe the Dems would put even more emphasis on this if they win and potentially turbo charge this sector.

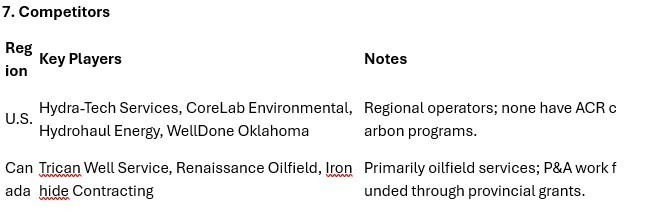

9. Oil-Service Stocks Context

The past year was flat for mainstream oil services. Schlumberger, Halliburton, and Baker Hughes posted record cash flows but stalled share prices. Rig counts held steady while maintenance and abandonment work became the quiet growth engine.

Mid-caps like Precision Drilling and Trican used their cash to enter environment services – a sign investors now value steady cleanup programs over volatile drilling cycles. Typical valuations remain only 3-5× EBITDA.

Zefiro is small, but its mix of services plus carbon recurring income gives it a better growth story than most. Over the next two years, ESG-linked government spend is set to rise, and for the first time the market is paying attention to companies that actually clean up the oilpatch.

APPENDIX-

BACKGROUND ON PLANT & GOODWIN PRE-ZEFIRO

Plants & Goodwin and Luke Plants – Background and Industry Context (Pre-Zefiro)

1. Company background: Plants & Goodwin (P&G)

Plants & Goodwin, Inc. was a privately held, family-owned oilfield services company founded in 1970, focused on plugging abandoned and orphaned oil and gas wells.

Core activities

• Plugging inactive and orphan wells

• Site remediation and environmental compliance work

• Supporting state and operator-driven cleanup programs

Geographic focus

Primarily the Appalachian Basin, including:

• Pennsylvania

• West Virginia

• Ohio

• Surrounding regions

Business characteristics

• Specialized service line:

The company focused narrowly on well plugging rather than offering a full range of oilfield services.

• Regional contractor profile:

Operations were concentrated in specific states rather than nationwide.

• Workforce scale:

Public disclosures suggest approximately ~100 employees prior to acquisition.

• Operating model:

Revenue came from:

• State-funded orphan well programs

• Contracts tied to regulatory obligations

• Project-based remediation work

Disclosure limitations

There is limited public information on:

• Revenue

• Profitability

• Market share

• Contract backlog

2. Luke Plants: Background and role

Luke Plants is part of the founding family and became the senior executive leading the company during its transition period.

Leadership role

• Served as CEO of Plants & Goodwin around the time of Zefiro’s investment (2023)

• Succeeded Steve Plants, who had previously led the company

Profile

Public information is limited, but his role can be described as:

• Second-generation leadership in a family-owned firm

• Responsible for continuing and managing a specialized oilfield services business

• Involved in operations within a regulated environmental services niche

There is little publicly available detail on his career outside the company prior to the Zefiro transaction.

3. Ownership transition to Zefiro

Timeline

• May 2023: Zefiro Methane Corp. acquired 75% of P&G

• 2023-2024: Luke Plants retained a 25% minority stake

• September 2024: Zefiro acquired the remaining stake and became 100% owner

Post-acquisition role

After the transaction:

Luke Plants transitioned into roles including:

• CEO of Zefiro Services

• Executive Vice President of Business Development

4. Industry structure before federal funding expansion

A. Market structure

Prior to major federal funding increases (pre-2021/2022):

• The well-plugging sector was:

• Fragmented

• Regionally organized

• Dominated by private contractors

B. Demand drivers

Demand came primarily from:

• State regulatory requirements

• Operator obligations (when responsible companies still existed)

• Limited state orphan well funds

Constraints included:

• Insufficient funding

• Irregular project pipelines

• Large backlog of unplugged wells

C. Supply characteristics

Contractors were typically:

• Small or mid-sized

• Regionally licensed

• Specialized in local geology and regulations

Barriers to entry:

• Technical knowledge

• Regulatory compliance

• Equipment and trained crews

Barriers were moderate, allowing many firms to remain small and local.

D. Regulatory structure

Regulation was state-specific, with:

• Different plugging standards

• Separate contractor approval systems

Limited federal coordination prior to 2021

This resulted in:

• No unified national market

• Strong regional segmentation

5. Industry shift in early 2020s

The Infrastructure Investment and Jobs Act (2021) allocated billions toward orphan well cleanup.

Effects included:

• Increased funding availability

• More consistent project pipelines (in the short term)

• Increased attention to methane emissions

• Entry of new participants, including public companies and investors

6. Position of Plants & Goodwin relative to peers

A. Compared to smaller contractors

P&G likely had:

• Multiple crews and equipment

• Ability to manage several projects at once

• Experience across varied well conditions

Smaller firms often:

• Operate fewer crews

• Rely more on subcontracting

• Handle shorter-duration projects

B. Compared to large oilfield service firms

Large companies (e.g., major oilfield service providers):

• Focus on active production services

• Typically do not prioritize orphan well plugging

P&G:

• Focused directly on plugging and remediation

• Worked within state-led cleanup programs

C. Compared to other regional specialists

Similar companies exist across the U.S. (Texas, Oklahoma, Appalachia)

P&G was:

• Comparable in scale to other regional specialists

• Not a national operator

• Primarily active in Appalachia

7. Economics of well plugging

A. Cost per well

Costs vary significantly depending on depth, condition, and location.

Examples from public data:

Ohio (2024):

• ~$60.7M spent for 412 wells → ~$147k per well

Ohio contracts awarded:

• ~$71.3M for 551 wells → ~$129k per well

Zefiro / P&G project:

• ~$4.5M for 37 wells → ~$122k per well

Texas discussions:

• Often cited around ~$30k per well

Variation reflects:

• Well depth and condition

• Site access and logistics

• Surface restoration requirements

• Regulatory standards

B. Contractor economics

Revenue characteristics:

Project-based or per-well contracts

Tied to government or operator funding

Cost drivers:

• Labor and crew utilization

• Equipment ownership vs. rental

• Materials (cement, casing, etc.)

• Transportation and mobilization

• Weather and delays

Uncertainties:

• Funding cycles

• Payment timing

• Project complexity

There is limited public data on margins for P&G specifically.

8. Industry consolidation and scale

A. Pre-consolidation state

• Highly fragmented

• Limited mergers or roll-ups

• Mostly independent regional operators

B. Emerging consolidation

• Early-stage consolidation began in the 2020s

• Driven by:

• Increased funding

• Interest from investors

• Carbon credit opportunities

C. Zefiro’s role

Zefiro’s acquisition of P&G:

• Converted a family-owned contractor into a subsidiary within a public company

• Provided Zefiro with in-house field operations capability

However:

• The broader industry remains fragmented

• No clear national leader has emerged

9. Carbon credit model (post-2023 context)

This is distinct from standard plugging contracts.

A. Process

1. Identify methane-leaking wells

2. Measure emissions before plugging

3. Plug the well

4. Verify emission reduction

5. Convert reductions into carbon credits

6. Sell credits in voluntary markets

B. Methodology

The American Carbon Registry (ACR) published a methodology in 2023

Defines:

• Measurement requirements

• Additionality rules

• Verification processes

C. Example

Zefiro reported a credit sale tied to:

• ~92,956 tonnes of CO₂ equivalent

• A project in Oklahoma

D. Key dependencies

The model depends on:

• Accurate methane measurement

• Regulatory acceptance

• Verification standards

• Market demand for credits

• Credit pricing

It does not apply to all wells or all plugging projects.

10. Overall summary

Before Zefiro’s involvement:

Plants & Goodwin was a regional, family-owned contractor specializing in plugging abandoned oil and gas wells, with a long operating history but limited public financial disclosure.

Luke Plants is the second-generation leader, managing the company during its transition to partial and then full acquisition.

The industry was:

• Fragmented and regional

• Dependent on state-level funding and regulation

• Characterized by irregular demand and limited consolidation

In the early 2020s:

• Federal funding increased activity levels

• New business models (including carbon credits) began to emerge

• Companies like Zefiro started acquiring contractors to build integrated operations