Articles

See All

The Energy Trade Few Investors Understand-For Good Reason

I made some of my biggest money EVER on ethanol business.

That happened in 2014, when the combination of government subsidies and a shortage of ethanol fuel led to massive margins for the ethanol business.

In a short amount of time, just months I think, stocks like Pacific Ethanol, now Alto Ingredients (ALTO – NASDAQ) became 8-baggers.

There is nothing I’d like more than the opportunity to do that again.

That experience has left me on the lookout for another run from the ethanol complex.

I thought that might be what we are the cusp on today.

The Iran war is sending up oil prices every day. As oil goes, so goes gasoline. And higher gasoline prices make fuel switching to higher ethanol blends more attractive.

On top of that, the ethanol producers are seeing another windfall from an unlikely source – the US Federal Government. In 2026 these companies stand to benefit big time from raised levels of 45z government credits.

The charts Green Plains Resources (GPRE – NASDAQ) and Alto Ingredients both look pretty good.

Source: Stockcharts.com

These companies have a wind at their back. Yet this isn’t a trade for the weak of heart! While the stocks can (and have!) do well, without these tailwinds the underlying ethanol business would be struggling to break even. That is likely going to cap any gains, and makes this a trickier bet going forward then I would like to see.

GREEN PLAINS AND ALTO –

THE GOVERNMENT DELIVERS

BLOW OUT RESULTS!

Green Plains reported Q4 2025 results in February. Alto reported their Q4 results just this week.

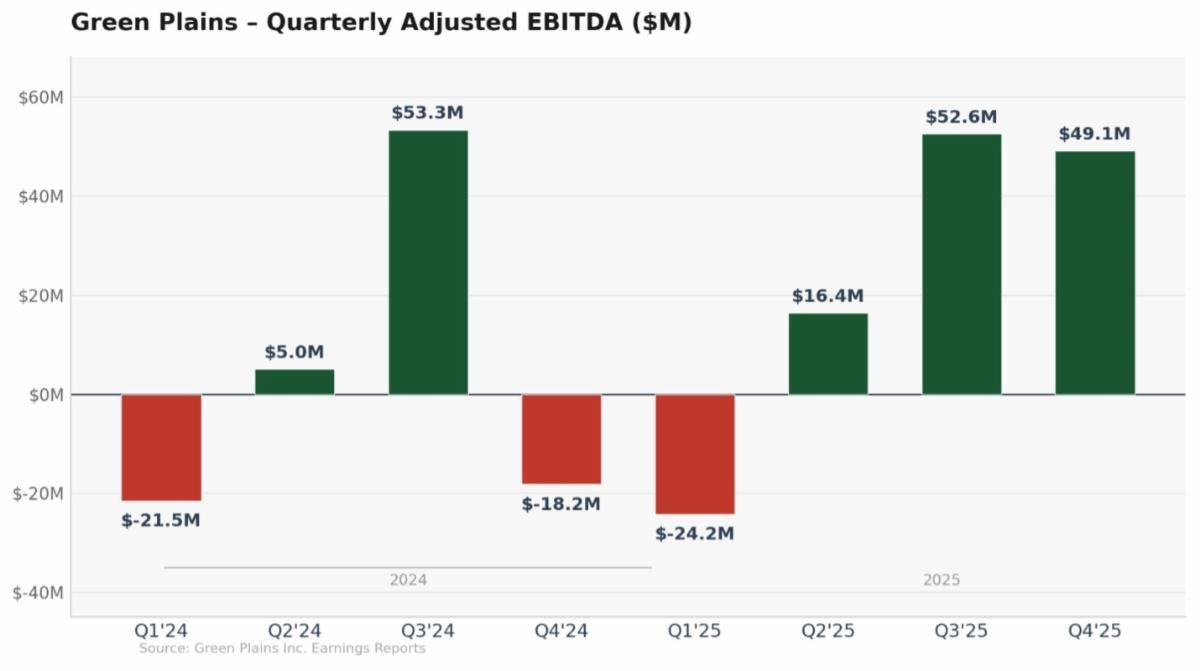

Green Plains saw net income of $11.9 million, or $0.17 per share, a huge improvement over a $55 million loss a year-ago. They also had adjusted EBITDA of nearly $50 million.

The story came down to clean fuel credits. More than half of Green Plains Q4 EBITDA came from the 45z clean fuel product credit. In 2026, those credits are going to be an even bigger part of earnings.

Alto did Green Plains one better. They had adjusted EBITDA of $28 million, which is a higher number than the past 7 quarters combined. 30% of that came from credits.

Both the stocks have rallied. Alto has seen its share price nearly double since reporting!

I do think these rallies are warranted. After all, Alto Ingredients is still priced at around 5x P/E (though they have about $280 million of debt as well).

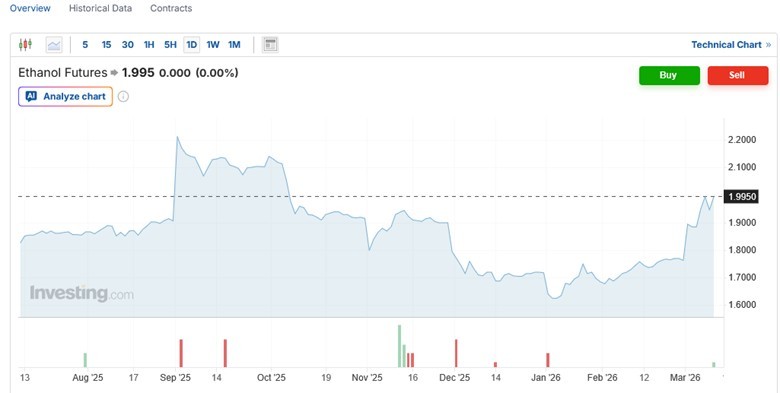

Both companies may see even better results going forward. Ethanol prices have reversed their seasonal weakness since the first missiles were launched targeting Iran.

Source: Investing.com

The only problem with this picture is that if you strip away the credits and strip away the war, the underlying ethanol business doesn’t seem particularly robust.

I will get to that in due time. But first, let’s talk about 45z credits. While the impact of war on ethanol is self-explanatory, the story of 45z credits is more complicated. Let’s dig into what they are.

WHAT IS 45Z AND WHY IT MATTERS

45Z is named after the section of the Inflation Reduction Act where clean energy production credits are defined.

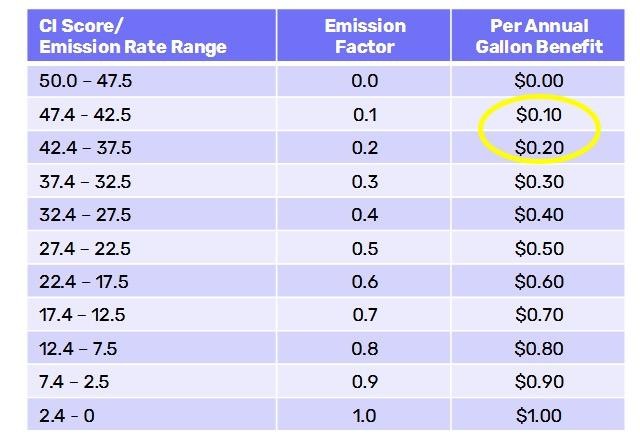

The section contains the details of a clean fuel production tax credit that gives ethanol producers a per-gallon tax credit based on the carbon intensity (CI) of the fuel they produce.

The CI score is based on the production methods used by your ethanol plant. US Treasury sets the criteria. Producers like Green Plains and Alto provide data about inputs, energy sources, and logistics of each of their plants, and the Treasury ranks it on a scale.

Source: Alto Ingredients

The lower your CI score, the bigger the credit.

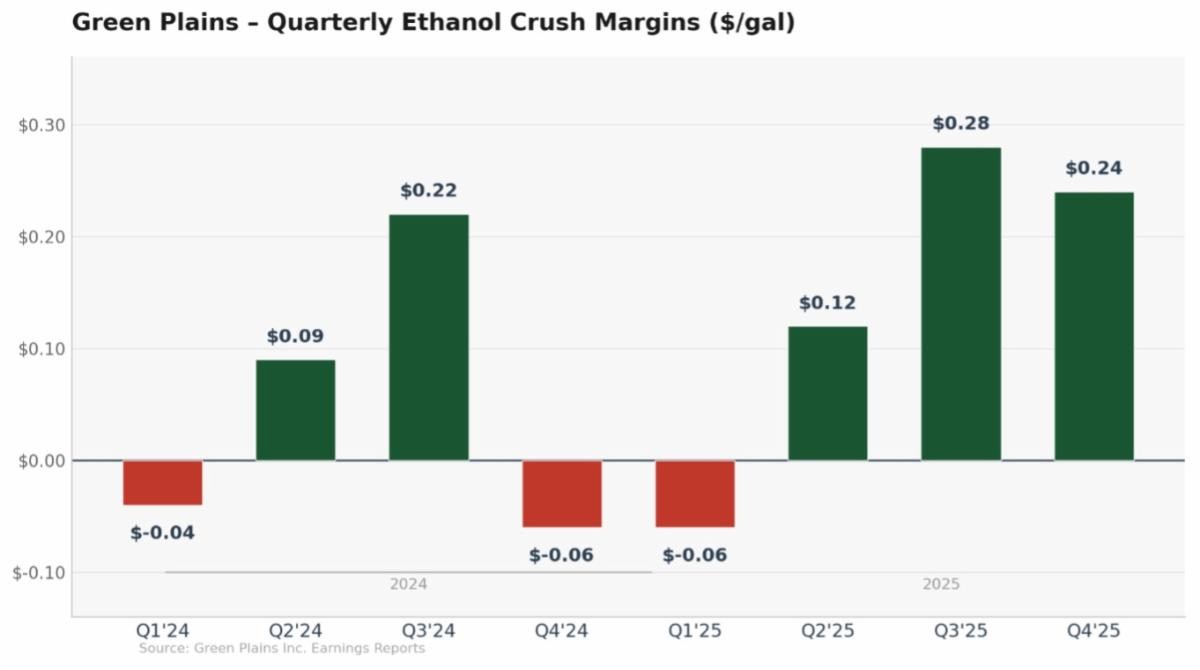

For fuels like ethanol, that credit can be up to $1.00 per gallon. That would be a massive number when you consider that ethanol crush margins have been hovering around 5 to 10 cents per gallon in recent years. Consider Green Plains crush margins over the last 8 quarters:

Source: Green Plains 10Q and 10K Filings

An ethanol plant might be grinding out 10-20 cents per gallon of margin on its production of ethanol. If that plant qualifies for a 45Z credit of, say, another 20 cents per gallon, the economics change completely.

The credit isn’t just a nice tailwind – it becomes the entire earnings story.

2025 was just the first inning. Not all plants could claim credits. You needed certified CI scores, approved reporting systems, and for the highest-value credits, you needed carbon capture and sequestration (CCS) infrastructure actually up and running.

Green Plains saw 3 of its Nebraska plants qualify for 45Z in 2025 but its 5 plants outside Nebraska did not. Alto had only one plant, Columbia, qualify.

In 2026, both these companies are guiding to more plants that qualify for credits. And thanks to the Trump Administration, the benefit will be even bigger than in the past.

THE 45Z TAILWINDS from the obbb

As part of the One Big Beautiful Bill (OBBB) act, passed last year, the Trump Administration made changes to the 45Z credit. The biggest for ethanol producers was the removal of something called the indirect land use change (ILUC).

ILUC was a clause in the IRA that made ethanol dirtier on paper. It essentially treated the land used to make ethanol as land lost to forestation, and thus land that would have otherwise been sequestering some carbon already.

That loss was then subtracted from any carbon gains made by the ethanol operation.

The whole thing seems a little suspect to me, and I guess to the Administration, because come 2026 they are doing away with it entirely.

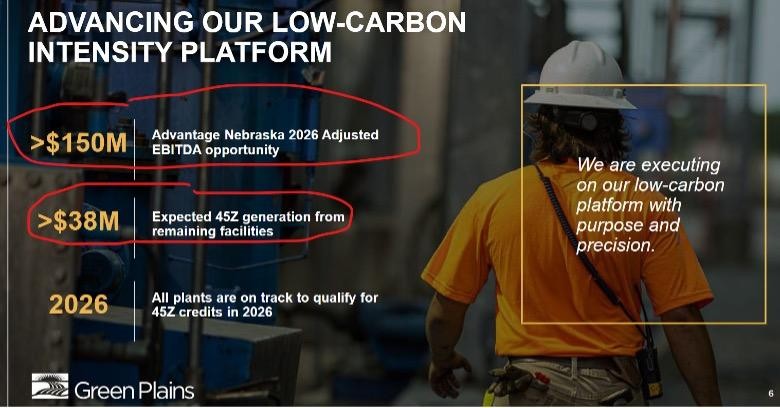

In 2026 Green Plain will see a number of plants that did not qualify for 45Z previously now qualify for the credit. In 2025 Green Plains had 6 facilities generating credits. In 2026 all 8 facilities will qualify.

Source: Green Plains Investor Presentation

The Nebraska plants that Green Plains owns already qualify for 45Z credits, but the amount they receive will go up in 2026, both because they qualify for the full year and because they qualify for additional credits because of carbon capture.

Green Plains has carbon capture at all three of their Nebraska locations: York, Central City and Wood River. The most recent was at York, where they just started CCS in October 2025.

Adding carbon capture allows Green Plains to capture even more 45Z credits. The IRA gives $85 for each metric ton of CO2 sequestered.

Source: Green Plains Q4 Results Presentation

In total, Green Plains is projecting an additional $188 million of EBITDA from credits in 2026.

For Green Plains, that is a lot of EBITDA. Consider that quarterly adjusted EBITDA over the last two years has never exceeded $55 million in a quarter.

Source: Green Plains 8-K Filings

Alto expects both their Columbia and Pekin Dry Mill facilities to qualify for 45z credits in 2026. In Q4 Alto saw a $7.5 million benefit from credits, or 10c per gallon after monetization costs.

In 2026 Alto is expecting their qualification to rise to 20c per gallon, which will add $15 million of net income.

If that sounds like a windfall, that’s because, quite honestly, it is.

But unfortunately, it’s a short lived one, and not changing the economics of the underlying ethanol business.

BUSINESS IS GOOD, BUT “THE BUSINESS” IS JUST… OKAY

Before their earnings call analyst consensus had Green Plains adjusted EBITDA at $180 million for 2026.

With the guidance Green Plains provided for $188 million of EBITDA from 45Z credits alone, those estimates had to go higher.

Alto had net earnings for the full year 2025 of $13 million. Now they are calling for $15 million in 2026, from just 45Z credits.

For both of these companies, we are talking about a BIG impact to the bottom line. But if you read between the lines, the other story is about the precarious nature of the ethanol business.

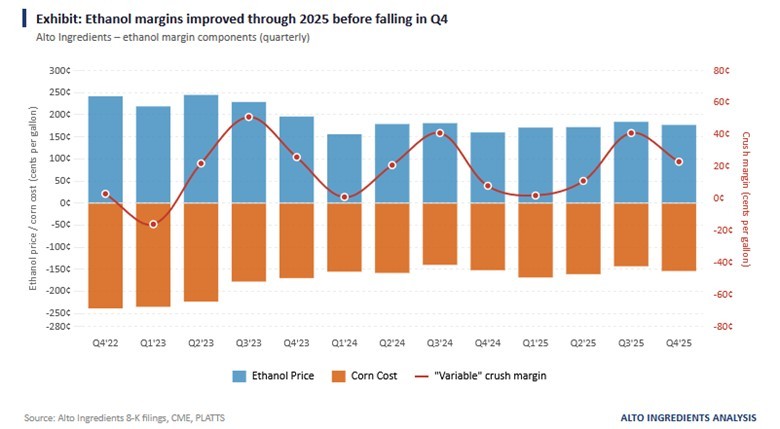

Ethanol has long been a business of barely breaking even. Below are Alto’s crush margins as ethanol and corn prices fluctuate.

The takeaway is that in the good times, margins get to maybe 50c pre gallon. And in the bad times, margins, and remember these are variable margins so not including the fixed costs of owning the plants, don’t pay the bills.

This is the real reason that 45z credits are such a windfall. It is because the underlying business is marginal at best.

The problem with this as an investor, is that stocks are all about discounted cash flow. The OBBB extends 45Z until 2029. While Green Plains and Alto get a benefit from 45z, it is only for 4 years.

That doesn’t make a huge dent in “the business” over the long run. It’s a dent, to be sure, but the stocks have already moved quite a bit.

Maybe the best thing these stocks have going for them is simply that they still aren’t expensive, even after big moves. They aren’t pricing in the “longer tail”.

Since Green Plains reported Q4 a number of brokerages raised their estimates for 2026.

Analysts raised estimates for mid-20c EPS to 38c for 2026. That number rises to 70c EPS for 2027.

Alto’s excellent fourth quarter result did much the same. Alto didn’t give 2026 guidance outside of the $15 million from credits. But EPS estimates from analysts have been raised – to 23c per share for 2026 and 35c for 2027. EBITDA is up to $45 million this year and $55 million next. Before earnings, those numbers were lower to the tune of $10 million.

With an enterprise value of $580 million, Alto trades at 10x next year’s EBITDA. Green Plains trades at about 7x EBITDA.

These are not expensive valuations. And you can make the case that the stocks could move higher.

But the question is how much?

Here’s the rub. Let’s consider Green Plains beause I can access the analysts own numbers. After Green Plains reported their Q4, BMO Nesbitt Burns raised their estimate of 2026 EBITDA by a whopping $96 million, or a 70% increase.

But almost 80% of the EBITDA is expected to come from 45z credits.

That means that the underlying ethanol business was only expected to generate about $50 million of EBITDA. Which isn’t a lot for a $1.4 billion enterprise value.

On top of this you can now layer better ethanol margins as long as the war is fought and gasoline prices stay up. But again, how sustainable is this?

In this way the ethanol stocks suffer from the same problem as the oil producer stocks. No one is going to pay up for surge pricing if they don’t think it will stick.

THREADING THE NEEDLE

With that said, these stocks could be a good trade as a bet on a prolonged, but not devastating, war.

I make the distinction between prolonged and devastating because if oil goes high enough to cause a recession, that is not going to be good for anyone, ethanol producers included.

If oil can remain elevated, keep gasoline high and giving good margins to ethanol, well… you could hit a sweet spot of fat margins and big earnings on what are already reasonable valuations.

You would be threading the needle.

But even so, what we are talking here is strictly a trade. For a bigger move (remember, I was looking for another 10-bagger) what these companies really need is a turn in ethanol fundamentals.

For now, there isn’t a lot of reason to believe we will see a second resurgence of ethanol.

Which means it looks like my dream of another ethanol windfall like the one in 2014 is not going to happen again.