Articles

See All

The Top E&P Team In The Most Profitable Play

NGX ENERGY INT’L

GASX-TSXV/PENYF-PINK

What happens when you

- get one of the most successful management teams in junior E&P history

- working in the most high margin oil and gas plays in the world

- just as they are starting out

I’ll tell you. You get the best ground-floor oil and gas stock I’ve seen in five years.

It’s a simple, easy-to-understand story with a management team who have made early stage shareholders rich in the past.

Ron Pantin is the Executive Chairman of NGX Energy Int’l Corp–GASX-TSXv—which has assembled a land package of natural gas assets that could see them be one of the largest producers in Colombia in a very short time. Federico Restrepo joins him as President.

Colombia has some of the highest natgas prices in the world now—contracts in the US$5+/mcf range and spot prices as high as $7/mcf—and the fundamentals suggest it could get even better with time. There is no volatility in pricing. It’s a producer’s dream!

This team knows what they’re doing. They’ve done this before—in Colombia. As the senior management of Pacific Rubiales—a Colombian oil and gas play—they grew the company from 14,000 bopd to 330,000 bopd in just four years.

In my 12 short years in oil and gas, I can tell you there has not been another growth story that comes anywhere close to that. Pantin’s team oversaw and managed that growth.

The stock ran from $2 to $34 over a little more than 2 years.

Now, most of the Pacific Rubiales team is back together here–and ready to grow just as quickly.

Way back in 2006, Rubiales started in much the same way as NGX is doing now. They acquired a large land package and made a discovery—in that case a gas area in northern Colombia called La Creciente.

La Creciente turned out to be the second largest field in Colombia.

The first well Rubiales drilled into La Creciente hit on 90 MMscfd. The stock price soared from 30c to $7.00 nearly overnight.

NGX has a better story. La Creciente was remote. Infrastructure was sparse – there was nothing there. I’ll show how you NGX’s land blocks each have gas pipelines with available capacity nearby.

The Macro Set-Up:

Colombia Needs More Natural Gas!

Everywhere in the world it seems that natural gas supply is abundant and cheap. But not in Colombia! It is now one of the most profitable locations on earth for producers.

That’s due to a few factors—both declining supply and increasing demand. But here’s The Big Story:

One of NGX’s neighbors has been one of the largest gas fields in Colombia – Chuchupa.

Chuchupa has been producing gas for 35 years. It accounts for 40% of Colombia’s daily natural gas production—and it is declining!

Ecopetrol, which owns Chuchupa along with Hocol, said last month that the production decline would reach 17% by 2022.

Bad news for Chuchupa is good news for NGX. There will be no problems with pipeline capacity. A nearby transmission line is only 14 kilometers away from NGX’s block.

Not only is natgas production around NGX’s land package declining, it is going down across all Colombia.

Proved gas reserves have nearly halved from their peak in 2009.

The country is in desperate need of gas. Demand is forecast to continue to trend up.

The country needs to replenish its natural gas reserves. The government knows this.

Big legacy fields like Guajira (~19% of Colombia’s natural gas production) and La Creciente are also in terminal decline.

Without the development of new basins and new reserves, natural gas production will continue to fall.

The Colombian government has indicated that natural gas will need to be the transition fuel for the country.

They expect to use more natural gas, not less, as the country moves toward a sustainable, green future.

The UPME (Ministry of Mines and Energy) projects that natural gas demand will increase from ~18% of total energy demand to 25% by 2040 and 34% by 2050.

What this means for NGX – and all Colombian producers – is higher prices.

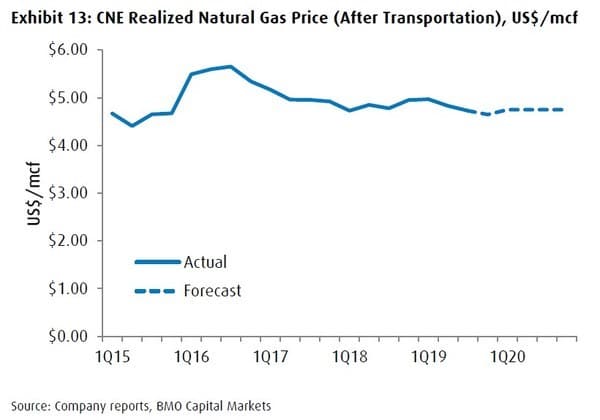

While natural gas markets in North America have been stuck below US$3/mcf for years, Colombian prices have averaged near $5/mcf.

Canacol (CNE-TSX), one of the largest natural gas producers in the country, has seen stable (and profitable!) commodity prices for over 5 years.

NGX COULD BE LARGEST PRIVATE SECTOR

NATGAS PRODUCER IN COLOMBIA: PANTIN

When a proven team makes a discovery, it can quickly add A LOT of shareholder value. The Market trusts that they will be able to raise the money and execute on a development drill program quickly—so the Market gives them credit in advance.

That happens all the time in a bull market. When a great team in Canada hits on a new play, the stock moves up. Same thing here.

It’s rare that retail investors get a chance at a team like this just weeks before the first drilling starts—usually the cheap, early stage money just goes to friendly institutional money or family money.

I’ve had some of my best wins in Colombia—Pacific Rubiales was huge and Petrominerales was a triple in nine months, from $11 – $33.

Colombia’s great geology means wells often pay back their costs very quickly–allowing junior producers to re-invest that money into new wells–and grow production within cash flow.

That means Free Cash Flow, no dilution and reducing debt as you grow.

Colombia can be a money-maker for investors.

NGX has 3 onshore blocks–all are prospective for natural gas and all have plenty of upside.

I only have room/time to talk about two—both are very large potential.

SN-9 – A Potential Company Maker

SN-9 neighbours Canacol’s big producing property to the east. NGX has a 72% participation interest in the block.

Source: NGX Investor Presentation

Canacol is producing a little over 200 MMscfd from these 3 neighbouring blocks. In Canacol’s most prolific field, Clarinete, wells have been tested in excess of 40 MMscfd.

NGX is about to start drilling the SN-9 property. The seismic tells them that the gas is there. A well drilled by Ecopetrol in 1992 on the block, the Hechizo-1, tested at 10 MMscfd.

The initial focus will start off by offsetting the Hechizo-1 well. 3-D seismic, followed by two to four exploration wells.

These are not deep wells – only 6,000 feet. They cost $4.5 to $5 million to drill and complete. The NGX team describes the exploration risk as “very low”.

NGX believes that SN-9 could be big enough to be not only important to the company, but an important new source of natural gas to the country.

Full development of the field would be about 36 wells. They forecast full-field production of 180 MMscfd if successful.

Source: NGX Investor Presentation

That would put SN-9 on the same scale as Canacol’s fields, but candidly, the hope is that SN-9 is much larger. They are looking for numbers as high as 1 trillion cubic feet (Tcf).

Canacol has an existing gas line that goes to the coast 25 kilometers from SN-9. A second gas line going south – to Medellin and Cali, is planned by Empresas Públicas de Medellín, (EPM).

NGX is expecting to drill their first well within weeks! This property has the potential to be a company maker.

Tiburon – A Potential COUNTRY Maker

Tiburon is surrounded by gas giants. Chuchupa to the south. Orca is an offshore (650 m deep! That’s expensive!!) is a large prospective field to the northwest. Perla, a 16 Tcf field to the east. The block is actually part of the same basin as Chuchupa.

NGX is looking for big numbers at Tiburon. Pantin tells me, “if we have two TCF, we can go up to 400 million standard cubic feet per day just from Tiburon.”

Tiburon is an onshore prospect, on the northern tip of Colombia (10 – 40%).

Source: NGX Investor Presentation

SN-9 will not cost a lot to ramp production up. Tiburon is so much bigger however, that Pantin says they will find a multi-national partner to help develop it.

First however they will shoot some seismic and identify targets to maximize their valuation.

If exploration is a success, we are talking big numbers. Pantin says that internal estimates show production peaking at close to 400 MMscfd and sustaining that level for 10 years.

Source: NGX Investor Presentation

WHEN WAS THE LAST TIME

I BROUGHT YOU

A NATGAS STOCK?

It takes A LOT of factors to line up for me to bring you an oil and gas stock.

- It has to be the right team—because management is everything. They need to have built a winner before and made investors money

- It has to be the right play—highly profitable, good jurisdiction

- Cash flow has to be immediate—no remote wells that need pipelines and permits and years of waiting

I think I’ve got all that in NGX. Institutional money knows and likes this team.

Their first drill program S-9, is right beside Canacol’s best asset. High quality seismic has been shot. Investors could not ask for a better location.

The Big Upside in the Tiburon block will attract investors. It’s needed. There are very few (if any other) places that need more hydrocarbon production.

NGX has all the right pieces. To be fair, it’s still exploration. But I play the junior resource market for The Big Discovery, and I think this is the best natgas junior I have seen in years. I’m long 100,000 shares.

NGX Energy International management has reviewed and sponsored this article. The information in this newsletter does not constitute an offer to sell or a solicitation of an offer to buy any securities of a corporation or entity, including U.S. Traded Securities or U.S. Quoted Securities, in the United States or to U.S. Persons. Securities may not be offered or sold in the United States except in compliance with the registration requirements of the Securities Act and applicable U.S. state securities laws or pursuant to an exemption therefrom. Any public offering of securities in the United States may only be made by means of a prospectus containing detailed information about the corporation or entity and its management as well as financial statements. No securities regulatory authority in the United States has either approved or disapproved of the contents of any newsletter.

Keith Schaefer is not registered with the United States Securities and Exchange Commission (the “SEC”): as a “broker-dealer” under the Exchange Act, as an “investment adviser” under the Investment Advisers Act of 1940, or in any other capacity. He is also not registered with any state securities commission or authority as a broker-dealer or investment advisor or in any other capacity.