Articles

See All

CASH FLOW IS SET TO TRIPLE BUT THE STOCK IS FLAT

ARE INVESTORS ANTENNAE NOT OUT?

A MATERIAL CHANGE IN THE WORKS?

Baylin Technologies (BYL – TSXv) has announced what could prove to be a genuinely transformative acquisition for the business—tripling the EBITDA here in 2026. Shareholders here have had a tough five years, but this new acquisition could change things.

In November, Baylin announced that they had acquired Kaelus AB, a Swedish provider of next-generation antenna solutions, RF conditioning, synchronization and test and measurement equipment.

(Wireless networks only work as well as their antennas and RF front ends – the components that shape, filter, transmit and receive the radio signals.

This is where Baylin sits: they build the physical hardware that transmits and receives those signals.

That starts with antennas – Baylin designs and manufactures a wide range of in-building antenna’s, stadium antennas, antenna arrays, rugged industrial use antennas, and smaller embedded WiFi and IoT antennas. All of these are sold through their wholly owned subsidiary Galtronics.)

This acquisition has the potential to be 1+1=3. It’s accretive to Baylin’s bottom line today. Baylin paid $42 million for Kaelus, which is only 4.5× Kaelus’s 2024 EBITDA.

On a post acquisition webinar, CEO Leighton Carrol admitted that they were lucky to get Kaelus so cheaply. Kaelus was privately owned by an aging founder with the participation from a Venture Fund that was in the process winding down. Together this made for motivated sellers.

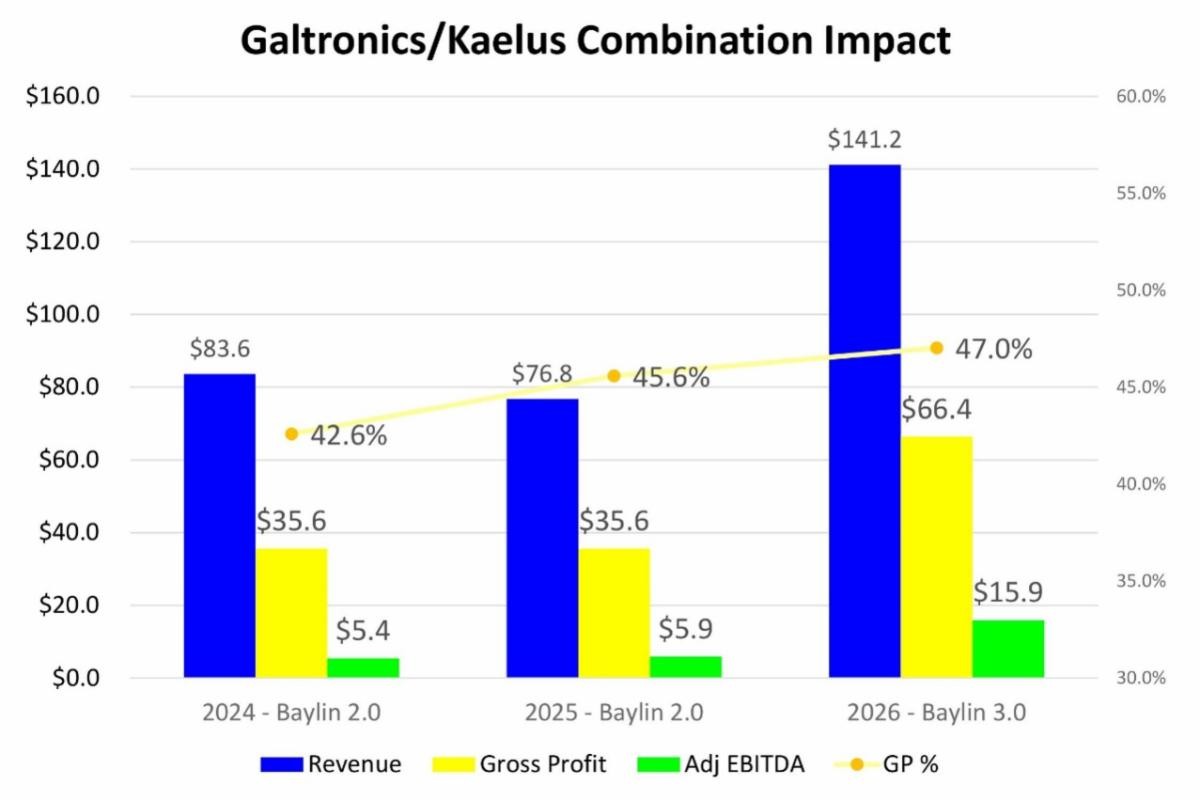

The acquisition is expected to make Baylin much more profitable today, with the potential for an even better future as synergies are realized.

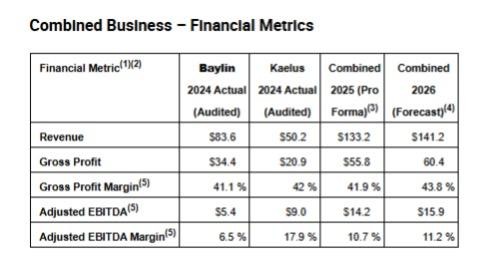

Even under conservative framing that assumes no synergies, Baylin expects adjusted EBITDA to more than triple in 2026!

Source: Baylin Nov 30, 2025, Press Release

That doesn’t mean there won’t be any synergies, just that Baylin can more than justify the acquisition without them.

If the company can execute anywhere near these expectations, the acquisition could mark a turning point – and the stock may finally be able to pull itself out of what has been a 6-year drawdown.

QUICK FACTS

Trading Symbols: CAD

Share Price Today: $0.28

Shares Outstanding: 254 million

Market Capitalization: $71 million

Cash: $5 million

Debt: $42 million

Enterprise Value: $108 million

THE COST OF CONCENTRATION

Baylin has been anything but an outperforming equity. There has been a half decade of value destruction.

Source: Stockcharts.com

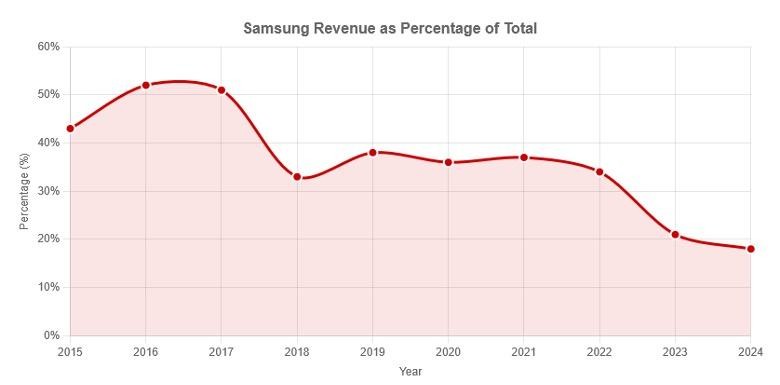

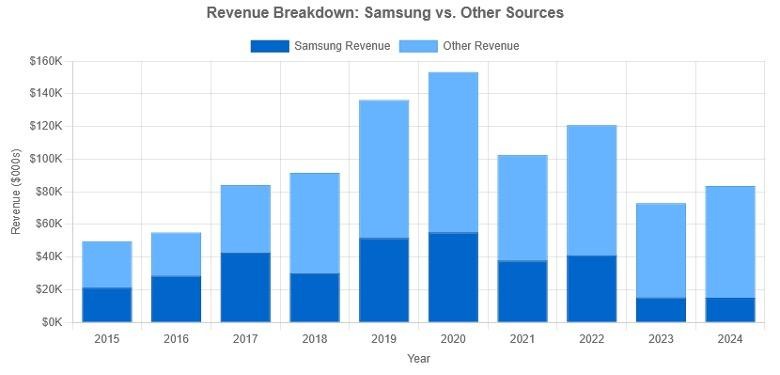

The root cause has been customer concentration. Baylin had long had a reliance on Samsung, which was as much as 50% of their revenue at the peak.

But since 2020 that relationship went south, and Samsung became a declining business.

Source: Baylin Disclosures

Source: Baylin Disclosures

That decline began in 2021. In 2020, Baylin’s Korea operations, which were largely dedicated to supplying Samsung, invested in a new factory to support the manufacture of MIMO antenna’s. That factory never ramped into meaningful production.

Baylin ran into more problems in 2022 when their major program with Samsung ended and a second supplier of Samsung antennae products was contracted.

To top it off, Samsung saw their own market share in smartphones declining.

In 2023 things hit rock bottom. Baylin saw their revenue decline from $121M to $73M. Their embedded / mobile antenna volumes, which were heavily dependent on Samsung, collapsed.

By late 2023 Baylin was in survival mode. In November of that year, they did a rights offering for existing shareholders. Every common shareholder received the right to purchase an existing share at 19c. The rights offering was 70% subscribed for 62.2M more shares, which raised $11.8M. This was enough to keep the lights on, but at the cost of heavy dilution to those shareholders who did not participate.

Baylin’s second step was to get rid of the embedded/mobile antenna business. Management hinted that this business was on the block through the first half of 2024. On July 9th Baylin announced an agreement to sell the unit to a strategic acquirer from Korea.

That sale closed at the end of 2024, which put an end to the dependency on Samsung and a renewed focus on the remaining RF and antenna related business.

By 2025, Baylin was no longer trying to grow its way out of trouble. It was focused on stabilization, repairing the balance sheet and resetting the trajectory of the company.

WHERE BAYLIN SITS

IN THE WIRELESS STACK

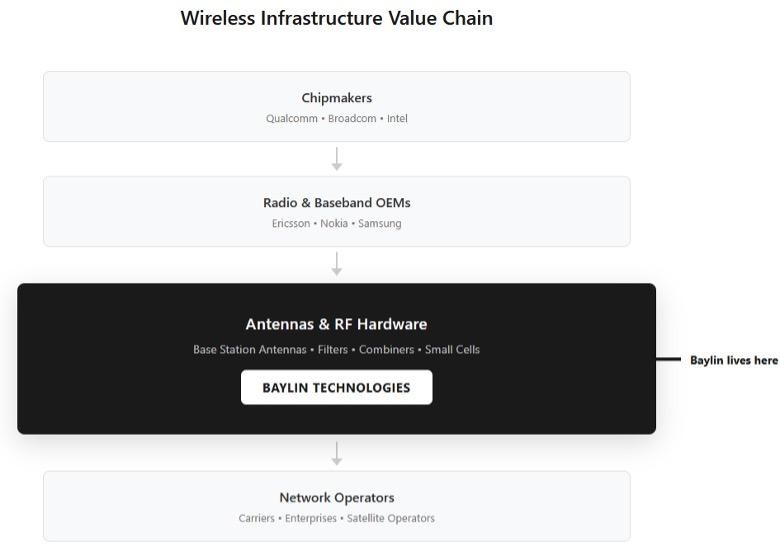

Wireless networks only work as well as their antennas and RF front ends – the components that shape, filter, transmit and receive the radio signals.

This is where Baylin sits: they build the physical hardware that transmits and receives those signals.

That starts with antennas – Baylin designs and manufactures a wide range of in-building antenna’s, stadium antennas, antenna arrays, rugged industrial use antennas, and smaller embedded WiFi and IoT antennas. All of these are sold through their wholly owned subsidiary Galtronics.

These aren’t fully integrated base station or small cell solutions.

Galtronics/Baylin is a component provider, and their business fits between the carriers and the OEM hardware sellers:

Source: Baylin Disclosures

Galtronics products are almost entirely geared toward the telecom carriers. Their customers are big carriers like Verizon, AT&T, Roger and Telus.

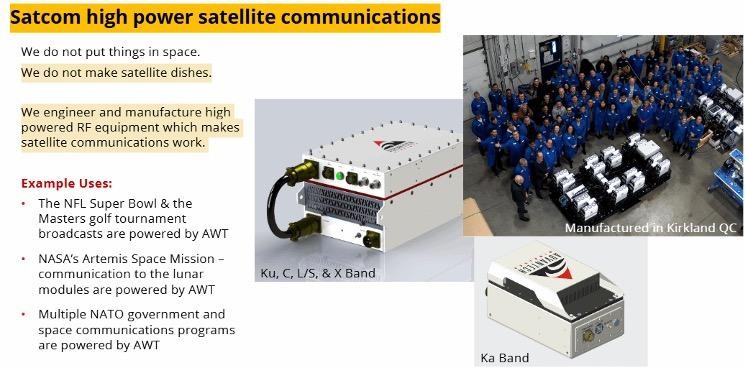

Baylin’s second business is Advantech Wireless. Advantech builds active RF equipment.

Advantech designs and manufactures amplifiers, they create integrated RF units by combining amplifiers with filters, power supplies and controllers, and they manufacture equipment for satellite communications.

Advantech also sells into the telecom vertical, but their products are used by the satellite industry as well.

Advantech doesn’t make the satellites, they make the RF equipment that creates, manages and amplifies signals between satellites and the ground.

Source: Baylin Jan 2026 Investor Presentation

Advantech does some sales to the defense industry. In the last few months Advantech announced a $2.5M contract for embedded antennas to be integrated into its next-generation body armour camera systems and another $1M contract for transceivers from a major US-based manufacturer of battlefield terminals.

Taken as a whole, the majority of the revenue for Baylin, including almost all the revenue from Galtronics, comes from telecom customers. Baylin doesn’t break out their defense business as a segment, but it is likely still small. Baylin’s satellite exposure is almost entirely through Advantech Wireless. That segment typically represents ~20–30% of consolidated revenue (it has fluctuated year to year).

HOW KAELUS CHANGES THE EQUATION

Kaelus is an RF equipment company, just like Baylin. But they are a complementary business, with not much overlap, both in the products that they provide and in the jurisdictions that they operate in.

Kaelus is headquartered in Sweden and has a big European presence, with additional exposure in India, China and Australia.

Baylin, by contrast, is heavily concentrated in North America. They sell to AT&T, Verizon, Rogers Bell, AT&T Mexico and Telus.

The only North American customer of Kaelus is T-Mobile.

From day one, the acquisition adds geographic balance rather than simply layering more of the same exposure.

Source: Baylin Webinar: Transformative Acquisition of Kaelus AB

The Kaelus customer base is also almost entirely wireless carriers. With Kaelus in the mix, Baylin’s consolidated customer base is expected to be 50% wireless telecom, 20% fiber/cable operators, 20% government and defense, and the remainder wireless enablement.

Baylin is hoping they can expand that reach to the broader wireless ecosystem, with tower companies like Crown Castle and SBA Communications, and with Shared Access and CellNet in Europe. These are all companies that already buy antenna products from Baylin, and they are the same people that would buy the RF conditioning and test and measurement equipment that Kaelus sells.

Baylin might have lucked into acquiring Kaelus at the right time. The acquisition cost $42M, which is 63.5% cash and 36.5% stock.

While what they paid was reasonable based on the 2024 numbers, Kaelus has seen their business grow since, making the acquisition look even more promising. Their backlog is up to $28M at the end of Q3. Some of the growth that Baylin is anticipating in 2026 forecast is coming from expectations of Kaelus.

In a surprising twist, because Kaelus is so profitable, Baylin’s debt leverage actually came down with the acquisition, even as they take on debt to complete it.

Strategically, Kaelus sits adjacent to Baylin’s fastest-growing end markets—wireless infrastructure, small cells, and dense venue deployments such as stadiums.

The product sets fit together naturally. Baylin, through Galtronics, supplies antennas for these deployments. Kaelus adds the RF conditioning, synchronization, and testing hardware that surrounds those antennas.

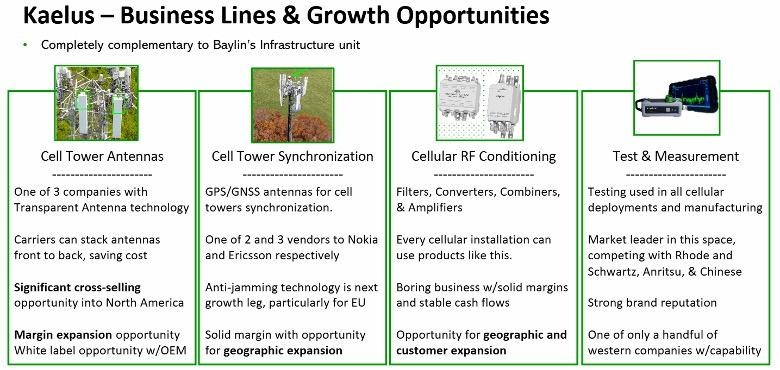

One gap in Baylin’s historical portfolio has been cell tower antennas. Kaelus fills that gap.

Kaelus tower antenna products have unique technology. They differentiate themselves through synchronization capabilities that address a practical economic problem for carriers. Telcos typically do not own the towers on which antennas are installed; they lease space.

Kaelus has developed technology that allows antennas to be stacked front-to-back on a single tower footprint, reducing the amount of leased space required. Only a handful of companies — including Amphenol and Huawei — offer comparable solutions.

Source: Baylin January 2026 Presentation

A second technology developed by Kaelus, in response to widespread GPS and network jamming linked to the war in Ukraine, is an anti-jamming technology. It has already been qualified by both Nokia and Ericsson. This technology is applicable beyond telecom – for instance, on a recent webinar Carroll said that it had been outfitted on military jeeps for testing.

Their RF Conditioning and Test and Measurement segments are not exciting growth businesses, but they make Kaelus a lot of money. These aren’t products that have a lot of proprietary technology, but every cell installation uses them.

A couple of weeks back, Baylin disclosed that closing of the deal was being drawn out a bit. I asked management about this, and it has to do with the Kaelus military business, which necessitates regulatory approval of the EU.

While Baylin expects approval, it could take more time depending on how quickly the EU moves on the request.

The strategic logic of the acquisition is straightforward: a shared customer base, adjacent products, and limited geographic overlap create multiple avenues for cross-selling. Baylin does not need heroic assumptions for the deal to work—but if even a portion of those opportunities materialize, Kaelus could prove to be more than just an accretive acquisition.

SET UP FOR AN IMPROVING 2026

The acquisition of Kaelus materially changes Baylin’s earnings profile. On management’s own numbers, the combined business is meaningfully more profitable than Baylin has been at any point in recent years.

Source: Baylin January Presentation

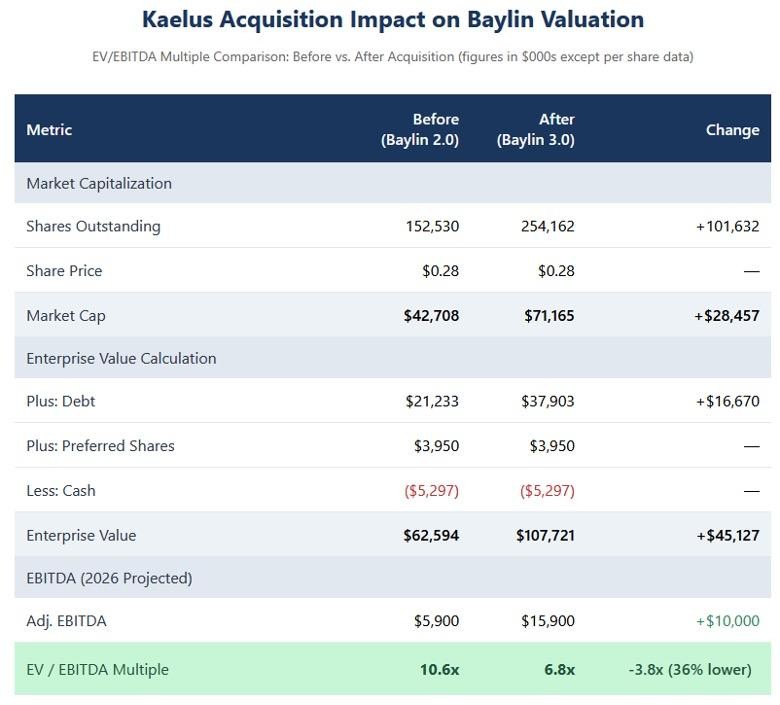

It also makes Baylin a much cheaper stock.

Source: Baylin Filings and Presentation Data

At the same time Baylin has worked its way through the year-over-year comps that came from selling their Mobile & Networking business. With that in the rear view, 2026 should be a much cleaner year.

Tariffs remain a wildcard, but not a big one. In 2025 Baylin, which produces a lot in China, was squeezed on tariffs. They worked hard through the year to mitigate the impact. Tariffs were still a 6% headwind to their US sales.

While I hope that won’t repeat in 2026, in today’s environment, nothing is certain about tariffs. Management has said that a breakdown of the Canadian-US free trade agreement would only impact their satellite business, which is manufactured in Quebec. They can mitigate any impact by shifting production to their US sister facility.

Tariffs do present some upside potential from Kaelus. Baylin did a lot of work last year restructuring their cost of goods sold, ensuring that the only items in the price of goods were the materials themselves. Doing this brought down the tariff impact a lot. Kaelus hasn’t gone through that sort of reconciliation (which is largely accounting).

As part of the acquisition of Kaelus, Baylin issued 52M shares. Those shares become free-trading in “9-24 months”. This could be an overhang down the road, but not right now.

Baylin also has Series A and B preferred shares that pay a 10% dividend.

The Series A preferred, of which there are $1.7M outstanding, are redeemable beginning Dec 2028 while the Series B preferreds, which total $2.25M, are redeemable Sept 2030.

Baylin has engaged a new lender to refinance their existing debt and the new debt needed to acquire Kaelus. They have signed a $31M term sheet. They expect the net debt to be under $30M.

When I first began digging into Baylin, I expected the satellite communications angle to be the most compelling part of the story, particularly given the enthusiasm around Starlink and AST Mobile.

That narrative doesn’t seem to apply here. The direct-to-device satellite systems largely bypass the land networks., and over time they could potentially be competition for Baylin (though Right now these are just separate end markets, targeting rural and out-of-reach cell service).

They are unlikely to become competition down the road because of the nature of their spectrum, which is terrible at penetrating buildings. But they don’t appear to be prospective customers either.

That leaves the Baylin “story” being primarily about a stabilized base of business buoyed the acquisition of Kaelus. This is not a story about chasing hype or betting on a new technology wave. It is a story about margin improvement, better product mix, and a cleaner corporate structure.

Which, after 6 years of losses, may be enough to rerate the stock.

DISCLOSURE–I have no position.

EDITORS NOTE–my last two junior resource stock picks continue to move up. Get the full reports with a risk free trial subscription–Click HERE:

Keith