Articles

See All

STEEL YOURSELF THIS CHART IS STARTING TO LOOK GREAT

QUICK FACTS

Trading Symbols: DRX

Share Price Today: $10

Shares Outstanding: 28.5 million

Market Capitalization: $285 million

Cash: $63 million

Debt: $39 million

Enterprise Value: $262 million

FROM TARIFF PUNCHING BAG TO CANADIAN INFRASTRUCTURE PLAY

Last year ADF Group (DRX – TSX) got hit by a wrecking ball.

Going into 2025, nearly 90% of ADF’s backlog was American work. American airports. American pharmaceutical plants. American commercial towers.

It was a good business — right up until tariff uncertainty froze the US construction market and turned ADF’s Canadian steel fabrication into a liability.

Steel fab is not a high margin business. When your plant isn’t full, you lose money. ADF used the Canadian federal work share program — where the government tops up wages for employees on reduced hours as an alternative to layoffs — to keep people employed. But there was no shielding the financial results.

The damage was severe. Revenue fell 24% in 2025. Gross margins collapsed by 44%. Net income dropped 53%.

It is a very bad year.

But ADF Group has fought back. They have dramatically decreased their reliance on US projects. They have strategically acquired distressed Canadian assets. They now look poised to carry the load for Canada’s infrastructure resurgence that the Liberal government is promising.

That could make the stock, which still largely reflects tariff uncertainties and has not yet embraced an infrastructure renaissance, an interesting play.

HOW THEY GOT HERE

ADF Group has been around for decades. They are very good at what they do.

Their flagship Terrebonne facility is one of the most automated, high-capacity steel fabrication shops in North America. It can process 125,000 tonnes of steel per year.

Their Great Falls, Montana plant adds another 25,000 tonnes.

ADF is capable of some of the most complex steel structures — they build massive skeletons for airports, office towers, pharmaceutical plants, and major infrastructure projects.

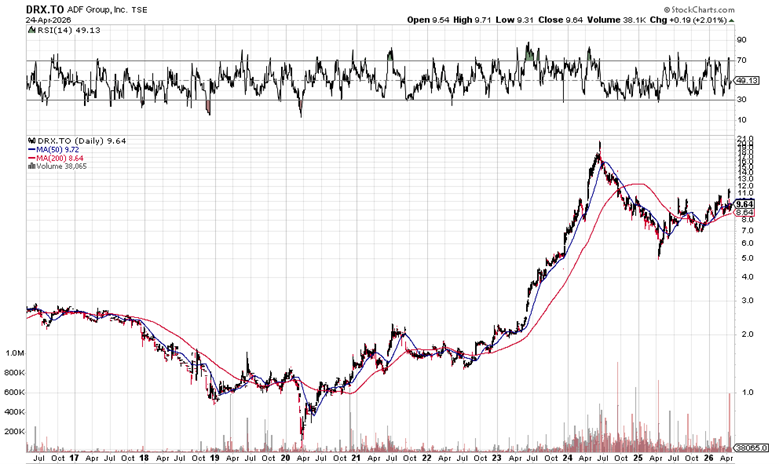

As the chart below shows, the last few years have seen the stock hit both the highs and lows.

Source: Stockcharts.com

After spending years as a single-digit stock, ADF went on a tear beginning in 2023.

That coincided with big infrastructure wins in both the US and Canada as governments and businesses spent on a post-COVID binge.

ADF benefited as major airports went through a generational investment cycle in 2022 to 2025. ADF won a number of structural steel contracts on airport terminals.

They also won a large contract from a pharmaceutical company, which almost certainly was Eli Lilly, as they built out capacity to satisfy the insatiable demand for their GLP-1 drugs.

These were big contracts – the Eli Lilly deal was well over $100 million. In 2024, just 4 customers accounted for 70% of ADF’s revenue.

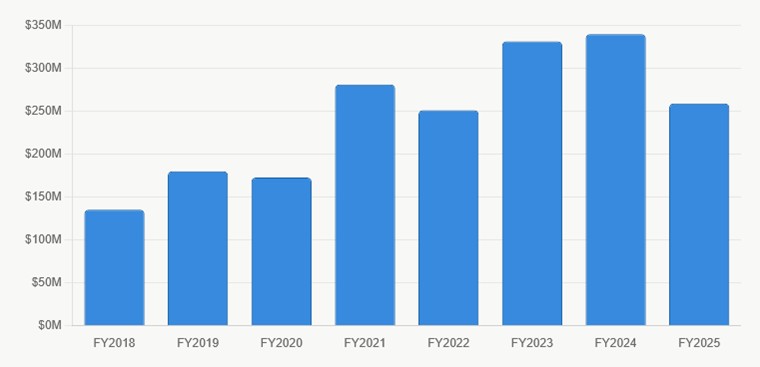

Altogether, the big wins led to a ramp in revenue, which crossed $300 million in both calendar 2023 and 2024.

Source: ADF Group Financial Disclosures

It could have been just the beginning. With AI taking off ADF may have been off to the races for even bigger gains.

But it wasn’t to be: their momentum was stopped in its tracks by Donald Trump’s tariffs.

A VICTIM OF THE TARIFF TANTRUM

Leading up to the Trump tariffs, ADF had a backlog that was nearly 90% in the United States.

While ADF operates facilities in both the US and Canada, their Terrebonne Quebec facility is the far bigger of the two.

Terrebonne has fabrication capacity of 125,000 tonnes of steel per year, while Great Falls is only about 25,000 tons. Which put ADF squarely in the crosshairs of tariffs.

The uncertainty caused US clients to delay signing contracts. ADF’s Terrebonne plant didn’t have enough work to keep its fabricators fully utilized. Steel fabrication is a high-fixed-cost business — your welders, your overhead cranes, your facility costs are all there whether you’re running at 100% or 70%. Underutilization crushes gross margin even at unchanged pricing.

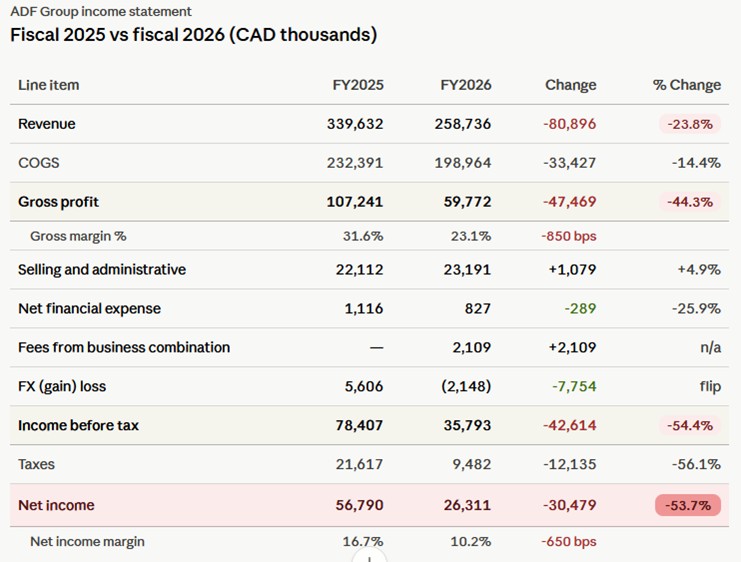

As a result, last year ADF’s results tumbled year-over-year.

Source: ADF Group Financial Disclosures

Revenue down 24%, gross margins down 44% and net income down 53%. Yikes!

GROUP LAR – PICKING UP DISTRESSED ASSETS ON THE CHEAP

ADF Group wasn’t the only Quebec steel company that struggled in 2025.

Groupe LAR, another Quebec based steel manufacturer, went into CCAA protection (that’s Canadian bankruptcy) in the summer of 2025.

The details are sparse, but it appears that Groupe LAR fell into a common trap of bidding on a fixed price contract that went on to far exceed their estimates of costs.

ADF acquired Groupe LAR out of bankruptcy in September for $20.4 million ($16.4 million cash plus $4 million in ADF shares).

LAR had generated $80.9 million in revenue in 2024. Paying roughly 25 cents on the dollar of revenue for a business with an established customer base and a $104.5 million order backlog is not a bad deal.

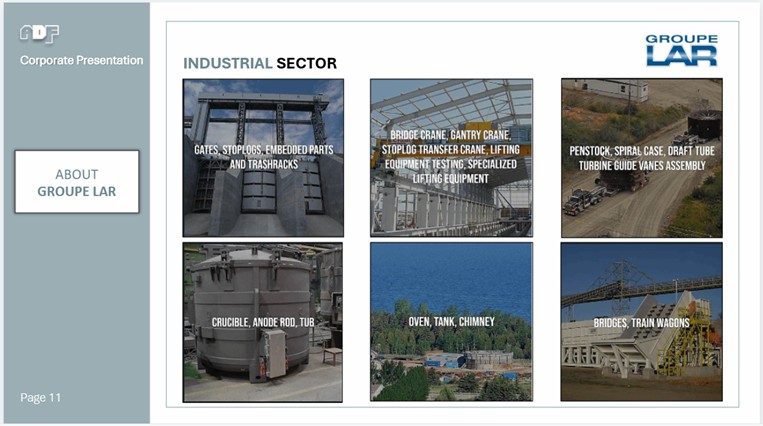

LAR is a turnkey steel structure fabricator. They operate in machining, welding, and industrial mechanics, and is a Canadian leader in the design, fabrication, and installation of mechanically welded steel structures.

Think turbine components, penstocks, hydraulic gates, spiral casings — the specialized mechanical infrastructure that sits inside Canada’s massive hydro dams. LAR also serves aluminum smelters, pulp and paper facilities, and other heavy industrial clients.

Source: ADF Investor Presentation

Most important, LAR is overwhelmingly Canadian in terms of their projects and backlog. Their focus is Hydro-Quebec and other Canadian hydro projects.

Source: ADF Group Investor Presentation

This could turn into a legitimate growth business. Hydro-Québec alone plans to invest more than $35 billion in hydroelectric dam renovation and new projects by 2035, with additional large-scale projects in Ontario, BC, and Atlantic Canada.

Ontario is planning to overhaul its hydro fleet with an investment of $2.5 billion.

British Columbia has a 10-year capital plan with $36 billion of investment in their hydro infrastructure.

At the time of the acquisition ADF saw a potential project pipeline of over $2 billion at LAR.

ADF plans to invest more than $35 million over 24 months to modernize and expand LAR’s main plant, with the goal of doubling LAR’s order backlog by January 31, 2027.

The goal is to get LAR margins up to the same as the rest of ADF Group. LAR’s gross margin was 10% in Q4. They are looking for a 1,000-1,500 bps improvement.

LET THE TURNAROUND BEGIN?

The Canadian government is preaching of an infrastructure renaissance. Count me a skeptic, but I am sure that if it happens, ADF Group will be a BIG-TIME beneficiary.

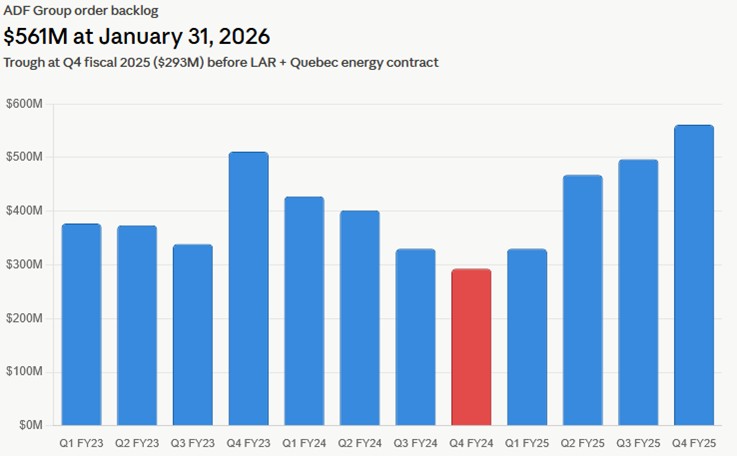

Even from the trickle of real work being announced so far ADF looks like a winner. They have announced a number of new contracts over the past few months and a big increase in their backlog. In just the last 4 months:

· On January 30th ADF announced “a series of new contracts in Quebec, Ontario and in the U.S. West Coast states totaling $140.0 million”. The work should run until the end of 2027.

· On April 8th, ADF announced more contracts, this time in Quebec and in the United States, worth $157.3 million. The biggest of which is a Groupe LAR contract for a hydroelectric project in Quebec.

The backlog stood at $561 million at YE 2026. The April contracts add to that further.

Source: ADF Group Press Release Disclosures

Of that $561 million backlog, 57% of it is made up of Canadian contracts. That’s a BIG change from just a year ago.

THE NUMBERS – IS THE BAD NEWS IN THE STOCK?

At $10, ADF Group has a market cap of $285 million and an enterprise value of $265 million.

ADF’s backlog is now bigger than it’s ever been. Yet while most of their backlog should be converted in a 12–18-month time frame, there are some wrinkles.

For example, there was a large $40 million energy contract that they signed last summer that is going to be completed over 5 years. Also, LAR’s portion of the backlog is $138 million, and those projects, big hydroelectric dams, are likely longer duration that ADF Group projects.

Nevertheless, getting back to a revenue level at par with their pre-tariff numbers doesn’t seem unreasonable. Revenue of $300 million to $350 million sounds do-able.

Add to that another $75 million from Groupe LAR and you are at $400 million for the entire business.

Groupe LAR is going to be a headwind on margins for at least a few quarters. ADF management said as much on the call. LAR bid for contracts at low margins before the acquisition and ADF has to honor those deals. LAR margins were only about 10% in the Q4 quarter, or less than half what ADF usually achieves.

Nevertheless, even at 15% corporate wide EBITDA margins, which would be well below the peak margins of 27%, that’s $60 million of adjusted EBITDA.

That values the stock at just over 4x EV/EBITDA valuation. On very conservative numbers. Which seems cheap for a business that seems to be getting back on track.

THE RISKS – THE TARIFF RISK WON’T GO AWAY

The downside? Well, the elephant in the room is and remains Trump and his tariffs.

On their Q4 conference call two weeks ago ADF management outlined the impact of the recently announced 10% steel content tariffs on any projects performed at Terrebonne. This new tariff will be added regardless of whether the steel used in the project comes from the United States or not.

Up until now, ADF’s Terrebonne projects for US customers went through a specific path — they bought US steel (so the fabricated structure can qualify for tariff exemptions or reduced rates as containing US-origin material), fabricated it in Quebec, and shipped it back across the border.

The new tariffs mean that workaround is now DOA. Terrebonne steel structures are going to get tariffed regardless of where the steel is from.

It is yet just one more challenge, and one more headwind.

But it’s the bigger picture that gives me pause. I mean: what next?

With the US-Canada free-trade agreement coming up for renewal in July, just a couple months away, there’s just so much uncertainty on how this plays out for ADF.

It could end up being a big positive. A deal and ADF could see partial or, in a perfect world, complete relief from the steel tariffs already imposed.

Or we could see a complete breakdown of trade talks and God knows what comes with that.

It won’t matter as much as it did. ADF is not the same business as it was a year ago.

But it still will matter to that US portion of the business.

The bet here is that ADF is simply cheap enough that the pros outweigh the cons. Especially given the infrastructure mandate that the Canadian Federal government is embracing.

That is no sure thing. But at 4x forward EBITDA, with a record backlog that is now majority Canadian, and a newly acquired business sitting in front of a $2 billion pipeline of hydroelectric infrastructure work — you are not paying much to find out.

Disclosure : Keith owns 2000 shares