Articles

See All

Another Oddball Commodity Play on Strait of Hormuz

![]()

If nothing else, the war has been a learning experience!

I have learned more than I ever cared to know about the supply/demand dynamics of obscure commodities that just happen to transit through the Strait of Hormuz.

At the top of that list… is sulfur.

Who knew that 40% of the world’s sulfur supply was squeezed through that tiny strait? Before the Iran war started, I sure didn’t.

The dislocation from the conflict has caused the sulfur market, and its downstream product sulfuric acid, to go on tilt. That has investors hunting for any company that stands to benefit.

One name that has crossed my desk more than once, is Ecovyst (ECVT – NASDAQ). With 110 M shares out, it has been listed since 2017—bottoming out last April at $5.50 and has now almost tripled in the last year—much of it because of the Iran war.

Has it run too far? Is this business truly inflecting here? Here’s my thoughts:

Ecovyst is the largest producer and the largest regenerator of sulfuric acid in North America.

On the surface, that sounds like the perfect setup for a war trade in a suddenly constrained commodity.

But as usual, the devil is in the details.

SULFURIC ACID –

SAME, SAME BUT DIFFERENT

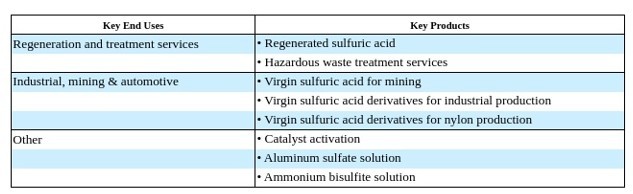

Ecovyst operates two different processes for producing sulfuric acid. But in practical terms, they produce one product that goes by two different names: virgin sulfuric acid and regenerated sulfuric acid.

Source: Ecovyst 10-K

The distinction is all about where the raw material comes from.

Regenerated sulfuric acid starts its life as used acid. Refiners use sulfuric acid as a catalyst in the production of high-octane gasoline. The acid isn’t consumed in the process, but it picks up impurities over time — water, organic residue from the oil — and gradually loses its catalytic properties.

The spent acid is a feedstock for Ecovyst. They strip it down at high temperatures and reconstitute it back into clean sulfuric acid. The refiner gets their acid back. Ecovyst gets paid a fee.

Virgin sulfuric acid is a different animal. Here Ecovyst buys elemental sulfur on the open market.

They incinerate the sulfur in furnaces to produce sulfur dioxide, then run it through the same oxidation and reformation steps to produce fresh sulfuric acid.

The product, which they call virgin sulfuric acid because it hasn’t been used yet, is sold to industries that can’t recycle the acid they use. These are operations like mining, fertilizer producers, paint manufacturers, battery producers, and nylon makers.

Ecovyst operates 8 regeneration and sulfuric acid production units in North America. These are located around refining hubs. They have four Gulf Coast units with two in Texas and two in Louisiana. They have another two units in California.

Source: Ecovyst Investor Presentation

Ecovyst also operates their Chem32 plant in Texas. This plant doesn’t have anything to do with sulfuric acid, though it does use sulfur containing gases to produce catalytic chemicals (RETAIL WON’T KNOW WHAT THAT IS—CAN YOU GIVE A SENTENCE TO EXPLAIN) that are used by refineries.

PASSING THROUGH THE COSTS

With that bit of background, we can parse out how Ecovyst is impacted by sulfur shortages and where the INVESTMENT thesis runs into trouble.

Ecovyst is fundamentally a manufacturer. They take a feedstock, which is either pure sulfur or the spent sulfuric acid, and produce a clean sulfuric acid product.

Unfortunately, that means any benefits that will accrue to Ecovyst are likely to be modest. Their costs are likely to follow market prices.

For the regenerated sulfuric acid business, which makes up most of their volume, they produce for refiners, and the contracts are structured on a cost pass-through basis.

Think of it like a tolling arrangement. The refiner provides the feedstock (spent acid). Ecovyst does the processing on a cost-plus basis. In fact, the refiner could (and sometimes does) choose to regenerate the sulfur themselves if they are willing to make the investment in the equipment to do so.

The regenerated sulfuric acid model Ecovyst offers is great for predictability. It is less great for leveraged exposure to a commodity price spike. The economics of regeneration are essentially agnostic to changes in sulfuric acid prices.

For virgin sulfuric acid, well the problem is even more straightforward. The Middle East shortages are sulfur shortages. Ecovyst is a bidder for sulfur feedstock, just like everyone else.

That’s not to say that there is zero benefit to Ecovyst. It is likely that Ecovyst will take advantage of the increase in sulfur prices to expand their margins, at least temporarily. And there is always the math of inflation – that the same margins at higher prices mean a higher dollar profit.

But that isn’t quite the windfall it would be if Ecovyst actually produced sulfur.

A FAIR VALUATION

Set aside the war for a moment and looking at the underlying business, what you find is actually pretty impressive — just not in a dramatic way.

Ecovyst has a market capitalization of $1.5 billion. They have about $400 million of debt and $200 million of cash.

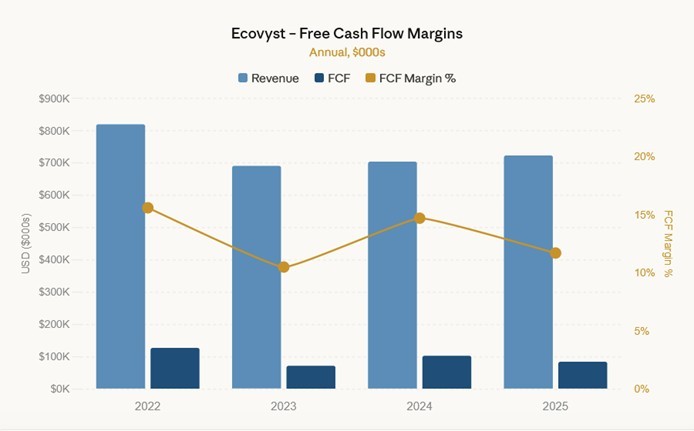

They operate a cyclical business, but one that has proven, reliable margins. Even as revenue fluctuates with sulfur prices, their free cash flow is remarkably consistent.

Source: Ecovyst Filings

Over the past four years, annual FCF has ranged from $72 million to $128 million, averaging around $97 million. That’s the hallmark of a company with real competitive advantages, which Ecovyst has. They are not just the largest but essentially the only scaled provider of sulfuric acid regeneration services in North America.

Their moat is real, and while refiner could theoretically bring regeneration in-house, it is capital intensive and Ecovyst has been doing this for so damn long.

At the current price of ~$13, Ecovyst trades at 18x FCF, a price I would call fair. If I thought that Ecovyst had significant upside from the disruption we are seeing in the Middle East, I would put the stock firmly in the “BUY” category.

But because the business is mostly passing through that sulfur price, I’m not sure the stock is worth a buy here. Especially given that it is up 20% since the beginning of the war. I worry that investors that were quick to pull the trigger on a “sulfur play” may be equally quick to the exit once the numbers begin to show their benefits are only modest to the bottomline.

But it is a good business. There may be other ways a clever management team could take advantage of this dislocation in the market. It will be worth watching the news flow to see what they can come up with.

If the stock comes back in, or if the company starts showing margin expansion that suggests they have figured out how to capitalize here, then this will be a name worth a harder look.